What Is Investor Due Diligence Analytics — and Why Do Most Startups Fail It?

Investor due diligence analytics is the practice of building your data infrastructure, metrics definitions, and reporting layer so that every number you present to investors is accurate, reproducible, and auditable — before the first term sheet arrives. Done right, it compresses the diligence cycle and builds confidence. Done wrong, it unravels deals.

Most growth-stage founders treat analytics as a fundraising task — something to "tidy up" when an investor asks for a data room. That is the wrong frame. By the time a lead investor requests cohort data, MRR reconciliation, or unit economics breakdowns, it is too late to build the infrastructure from scratch without red flags appearing in the process. The founders who close rounds faster and at better terms are the ones who have already built the plumbing.

This post is for founders, CFOs, and heads of finance at pre-seed through Series B companies who are either preparing to raise or have already learned the hard way that "the numbers are in the spreadsheet" is not an answer that holds up in diligence.

Why Investor Due Diligence Kills Deals That Should Have Closed

The problem almost never starts with the business. It starts with the data.

A pattern we see repeatedly when working with Series A-stage companies is that their headline metrics are real and defensible — but they exist in five different places, calculated five different ways, and none of those calculations are documented. When an investor's analyst starts pulling threads — "How is gross margin calculated here?" "Why does this cohort table show a different retention figure than the board deck?" — the answers either take days to produce or contradict each other.

That inconsistency is a deal-killer. Not because the investor thinks you are hiding something, but because it signals that the business is not ready to scale. If the data is this fragmented at Series A, what happens when there are 300 employees and five product lines?

The specific failure modes we see most often:

1. Metrics defined differently across systems. Finance calculates MRR one way. The product team pulls it another way from the product database. Neither matches what was in the board pack three months ago. There is no documented definition anywhere.

2. Spreadsheet-based reporting that cannot be audited. When an investor asks "Can you show me this broken down by cohort, by geography, for the last 24 months?", the answer should come from a data warehouse query, not a re-jigged Excel pivot table built at 2am. The latter introduces errors under pressure — and investors can usually tell.

3. No clean audit trail between source data and reported metrics. Investors doing serious diligence will want to trace a number all the way back to its source. If the path from raw transaction data to the headline metric runs through a manual step — a CSV export, a spreadsheet calculation, a VLOOKUP — that is a gap in the audit trail and a reason to pause.

4. Retention and cohort data that does not reconcile. This one catches almost everyone. Retention curves presented in pitch decks are often calculated on a subset of customers, or using a definition of "active" that is more generous than what the underlying data supports. When an investor recalculates independently — which the serious ones always do — the numbers rarely match.

For a deeper look at how retention calculations go wrong at the data layer, read our post on Cohort Analysis for Startups: Why Your Retention Numbers Are Lying to You.

📺 Watch: How to Pass Investor Due Diligence (And Close Your Seed Round)

What Investors Actually Look For in a Data Room — Beyond the Documents

The documents in a data room — pitch deck, financials, cap table, contracts — are the minimum bar. What separates a smooth diligence process from a grinding one is whether the underlying data that generated those documents is accessible, consistent, and reproducible on demand.

Here is what a data-literate investor or their diligence partner is actually evaluating:

Metric reproducibility. Can you run the same query twice and get the same answer? Can you run it for a different time period without restructuring your entire reporting setup? This requires a semantic layer or at minimum a well-governed set of SQL models — not a dashboard that someone manually refreshed last Thursday.

Definition consistency. Is "customer" defined the same way in your CRM, your billing system, and your analytics platform? If not — and in most early-stage companies it is not — you will spend half of diligence explaining discrepancies rather than selling the business.

Trend data at the right granularity. Investors want to see monthly cohorts, not quarterly summaries. They want to see gross margin by product line, not blended. They want to see CAC by acquisition channel, not total. If your data infrastructure cannot produce these cuts quickly, you will either delay the process or produce numbers you cannot fully defend.

Self-service access without needing an engineer. A finance or ops team that has to raise a Jira ticket every time an investor asks a follow-up question is a diligence liability. The infrastructure should allow a non-technical team member to answer reasonable data questions without developer intervention.

If you are looking at the infrastructure side of this problem — what it actually takes to build a stack that supports this kind of self-service reporting — explore how Fintel Analytics approaches this. We work with pre-seed through Series B companies globally to design and deliver exactly this kind of capability.

How to Build an Analytics Stack That Holds Up in Due Diligence

This is not about having the most sophisticated data infrastructure on the market. It is about having the right level of infrastructure for your stage — clean, documented, and auditable. Here is the framework we apply when working with companies preparing to raise.

Step 1: Centralise your source data into a warehouse

If your metrics currently live across Stripe, your CRM, a billing database, and three spreadsheets, your first task is getting all of that into a single, queryable place. For most Series A-stage companies, BigQuery or AWS Redshift is the right call — low operational overhead, scales without drama, and both integrate cleanly with the transformation and BI tools in the rest of the stack.

Do not skip this step or try to shortcut it with a "virtual" integration layer. Investors doing proper diligence will want row-level data access to validate your aggregates. If the rows do not exist in one place, you cannot provide that.

For guidance on when this infrastructure investment makes sense at your stage, see our post on When Does a Startup Need a Data Warehouse? A 2026 Guide.

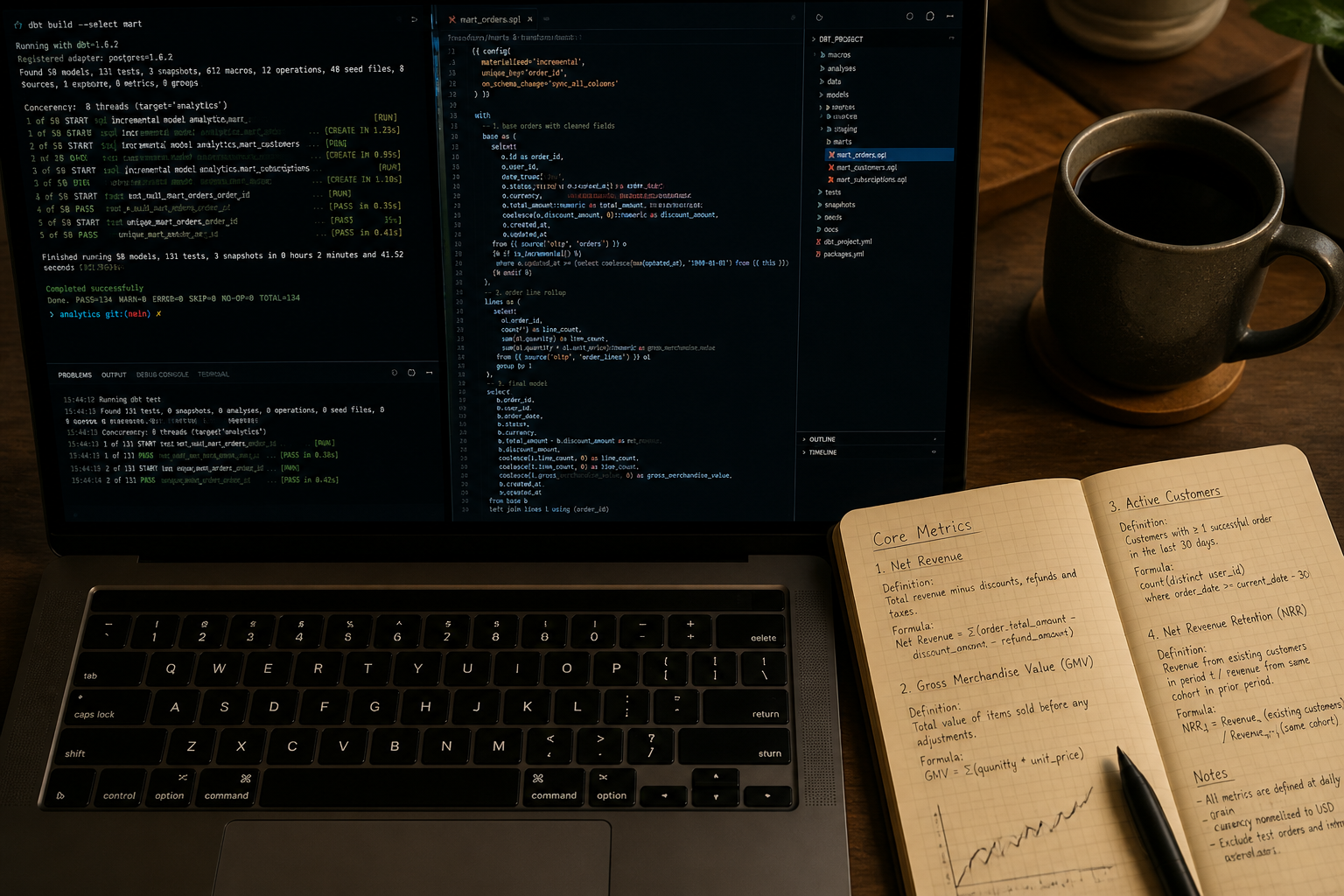

Step 2: Build your core metrics in dbt — not in your BI tool

This is the most common structural mistake we see in early-stage analytics stacks. Companies build their metric logic inside their dashboarding tool — inside Looker calculated fields, inside Metabase custom expressions, inside a Sheets formula — rather than in a transformation layer.

The consequence: when an investor or their analyst pulls the raw data and tries to reproduce your figures, they cannot. The calculation only exists inside the tool, not in the data itself.

Building your metrics in dbt models — gross margin, MRR, cohort retention, CAC, LTV — means the logic is version-controlled, documented, testable, and reproducible outside any specific dashboarding tool. When an investor asks "Can you share the SQL behind this?", you can. That level of transparency builds disproportionate trust.

In our work with a Series A payments company, migrating calculations from spreadsheets into dbt models eliminated a class of recurring manual errors and cut weekly finance maintenance time by 30 minutes — with the added benefit that every metric was now auditable to source data.

Step 3: Define your metrics formally — in writing

This sounds obvious but almost nobody does it before they have to. A metric definition document (or a metrics catalogue in your semantic layer) should answer for every reported metric: what is the precise calculation, what data source does it draw from, what edge cases are excluded and why, and who owns it.

When an investor asks "How do you define active user?" you should be able to point to a document, not reconstruct the answer on the fly. When two team members are asked the same question independently, they should give the same answer.

A SQL semantic layer makes this formal and enforced rather than aspirational. If you are not familiar with how this works in practice, our post on the SQL Semantic Layer: Why Your Metrics Are Broken in 2026 covers the architecture in detail.

Step 4: Build investor-ready dashboards before you need them

The dashboards you build for investor diligence should be treated as data products, not one-off reports. They need to update automatically, cover at least 24 months of history, and present metrics at the granularity an investor will want to drill into.

For most growth-stage companies, the essential set includes:

- Monthly revenue and MRR/ARR bridge

- Cohort retention by acquisition month

- Gross margin by product or segment

- CAC and LTV by acquisition channel

- Burn rate and runway with actuals vs. forecast

- Headcount and cost per function over time

None of these dashboards should require manual intervention to refresh. If your head of finance has to spend 90 minutes every week compiling the board pack from multiple sources, that is not a dashboard — it is a reporting process waiting to fail under diligence pressure.

We helped one fintech company replace exactly that process: weekly executive reporting that required 90 minutes of manual work was replaced by a live dashboard — zero manual effort, updated hourly. When that company entered a raise three months later, investor data requests that would previously have taken days were answered in minutes.

Step 5: Validate your numbers before investors do

Before you open a data room, run your own diligence on your own data. Have someone — ideally someone who did not build the models — attempt to reproduce every headline metric from raw source data. Note every discrepancy they find. Investigate every one before an investor does.

The reconciliation step is where hidden problems surface. In one capital reconciliation project we ran for a global fintech, a systematic discrepancy that had been invisible in summarised reporting turned out to represent a $25M gap — at market borrowing rates, costing over $6,000 per day. That is an extreme case, but smaller discrepancies — a few percent off in reported retention, a miscategorised revenue line — are common and damaging to investor confidence even when they are genuinely innocent.

The Real Cost of a Data-Unready Fundraise

The cost of getting this wrong is not just a slower close. It shows up in several concrete ways:

Extended diligence timelines. Data-unready companies spend weeks answering incremental data requests that a well-instrumented business could resolve in hours. Research from 2026 suggests that deals utilising modern, well-organised data environments close significantly faster than those relying on legacy, manual processes — with some estimates indicating an average difference of nearly two weeks in deal closure time.

Valuation haircuts. If investors cannot independently validate your metrics, they will either walk away or discount the valuation to compensate for the uncertainty. A business where the numbers check out commands a premium. A business where every answer requires a follow-up question does not.

Renegotiated terms post-LOI. One of the most damaging scenarios is where an investor issues a letter of intent based on your stated metrics, then discovers inconsistencies in diligence. At that point you are negotiating from a position of weakness — either correcting numbers that are worse than presented or explaining why the discrepancy is immaterial.

Reputational drag. Investors talk. If your diligence process was a mess, that observation follows you into the next round.

The companies that move through diligence cleanly are rarely the ones with the best underlying metrics. They are the ones with the best underlying data infrastructure. The metrics are a product of the stack — and the stack either holds up or it does not.

Frequently Asked Questions

Q: What analytics data do investors typically request during due diligence?

A: Investors typically request monthly cohort retention data, MRR or ARR with a bridge reconciliation, gross margin broken down by product or segment, CAC by acquisition channel, burn rate with actuals vs. forecast, and unit economics including LTV/CAC ratio. Data-literate investors will also request the underlying data or SQL logic behind headline metrics to verify reproducibility.

Q: How far in advance should a startup build its analytics stack before fundraising?

A: Ideally, 6–12 months before you expect to open a data room. This gives you time to centralise your data sources, build and validate your core metric models, identify and fix any discrepancies, and accumulate enough historical reporting that trend lines are meaningful. Building this under time pressure — after an investor has expressed interest — almost always produces errors and delays.

Q: What is the most common analytics mistake startups make before a fundraise?

A: Defining the same metric differently across systems — for example, calculating MRR one way in the finance system and another way in the product database. When investors see two numbers for the same metric and neither explanation is documented, it erodes trust in all the numbers, not just the ones in conflict.

Q: Do investors expect startups to have a full data warehouse before Series A?

A: Not necessarily a sophisticated one, but they expect the data to be centralised, consistent, and reproducible. A lightweight BigQuery or Redshift setup with dbt transformations and a clean BI layer is entirely appropriate for Series A. What raises flags is not the choice of tooling but the absence of auditability — metrics that live only in spreadsheets or dashboards that cannot be traced to source data.

Q: How does investor due diligence analytics differ from regular business intelligence?

A: Regular business intelligence is optimised for speed and usability — helping your team make decisions day-to-day. Investor due diligence analytics requires an additional property: auditability. Every number must be traceable to a documented source, reproducible independently, and consistent across every context in which it appears. This requires tighter governance, version-controlled models, and formal metric definitions — disciplines that improve your BI even after the raise is complete.

The founders who struggle most in diligence are not the ones with bad businesses — they are the ones with good businesses and broken data infrastructure that makes those businesses look worse than they are. At Fintel Analytics, we have helped fintech, payments, and SaaS companies build exactly the kind of analytics stack that survives investor scrutiny — from centralising raw data sources into a clean warehouse, through to dbt models, semantic layers, and investor-ready dashboards that update without manual effort. If your data room is held together with spreadsheets and hope, that is a solvable problem — and solving it before your next raise is one of the highest-leverage investments you can make.