Chargeback dispute analytics is the practice of building structured data pipelines, metrics, and models around your dispute lifecycle — so that instead of absorbing losses reactively, your team can identify root causes, optimise representment strategy, and prevent future disputes before they are filed. For fintech companies, payments platforms, and e-commerce businesses processing at scale, this is not a nice-to-have. It is the difference between treating chargebacks as a tax and treating them as a manageable operational risk.

The scale of the problem is stark. According to Mastercard's 2026 research with Datos Insights, global chargebacks are expected to grow 37% from 2025 to 2029, reaching 359 million transactions annually. For merchants in the United States, LexisNexis Risk Solutions data from 2025 shows that every dollar lost to fraud costs merchants $4.61 in total when fees, operational overhead, and lost merchandise are factored in. That multiplier is what makes chargebacks uniquely damaging — and uniquely worth instrumenting properly.

Most early-stage payments companies and e-commerce businesses are not doing that. They are logging into PSP portals, exporting CSVs, and managing disputes in spreadsheets. If that is your current setup, this post will show you exactly what to build instead.

Why Chargeback Data Is Almost Always Broken Before You Start

Before you can build analytics, you have to understand what you are actually working with — and the honest answer is that chargeback data is some of the messiest in payments.

The data arrives from multiple places simultaneously: your PSP or acquirer portal (often via manual export or a limited API), your internal order management or CRM system, your fraud tooling, and card network reason code classifications that differ between Visa and Mastercard. None of these sources use the same transaction identifiers. None of them are designed to join cleanly. And none of them update at the same frequency.

A pattern we see repeatedly when we start working with Series A payments companies is that their "chargeback report" is actually a spreadsheet built by someone in the finance team who exports from three portals every Monday morning, pastes the data into a master tab, and manually deduplicates by transaction amount and approximate date. That person leaves, or goes on holiday, and the business goes blind.

The first step in building real chargeback dispute analytics is not choosing a BI tool — it is mapping every data source in the dispute lifecycle and establishing reliable, automated ingestion for each one. That means:

- PSP dispute webhooks or scheduled API pulls into your data warehouse (BigQuery or AWS, depending on your stack)

- Order and customer data from your core platform, joined on a stable transaction or payment reference

- Fraud signals — device fingerprints, velocity flags, risk scores — at the transaction level

- Network reason codes normalised across Visa and Mastercard schemes (they differ materially, and lumping them together destroys the analytical value of either)

Once those sources land in your warehouse and are modelled in dbt, you have something you can actually reason about. Until then, every metric you produce is provisional.

📺 Watch: Chargebacks - An Overview of the Representment Process

What Metrics Actually Matter in Chargeback Dispute Analytics

The default metric most teams track is overall chargeback rate — disputes as a percentage of total transaction volume. It matters, because exceeding Visa's VAMP threshold (which dropped to 0.9% from January 2026) triggers fees and acquirer scrutiny. But it is a lagging indicator, and by itself it tells you almost nothing about where to intervene.

The metrics that actually drive decisions are:

Chargeback rate by reason code — this is the single most actionable segmentation you can build. A spike in "goods not received" chargebacks from a specific fulfilment region tells you something entirely different from a spike in "unauthorised transaction" codes across a particular BIN range. Without this breakdown, your operations team is responding to aggregate noise.

Win rate by reason code and dispute category — as of 2025, US merchants win an average of 54% of chargebacks they contest through representment across all dispute categories. But that average obscures enormous variance: win rates for fraud-related chargebacks average just 17.1%. If your representment strategy does not account for this, you are almost certainly wasting effort fighting unwinnable cases while under-investing in the ones you can recover.

Dispute value concentration — which SKUs, customer segments, or transaction corridors are generating outsized chargeback value? A global fintech we worked with discovered that 12% of their merchant IDs were responsible for over 60% of their dispute value. That concentration was invisible in their overall chargeback rate, but immediately actionable once modelled at the merchant cohort level.

Pre-dispute alert coverage — tools like Verifi and Ethoca allow merchants to intercept disputes before they become formal chargebacks by issuing a refund pre-emptively. Your analytics need to track what percentage of your dispute volume is being caught at this stage and what is slipping through to full chargeback.

Recapture rate — how much of your dispute losses are you actually recovering through representment, net of the cost of fighting? Industry data from 2025 shows average recapture at 62%, while best-in-class operations reach 95% — a gap that represents millions of dollars for any mid-sized payments business.

If you are looking to implement this kind of dispute intelligence in your organisation, explore how Fintel Analytics approaches payments data — we work with fintech and payments businesses globally to design and deliver exactly this kind of analytics infrastructure.

The Friendly Fraud Problem Requires a Different Data Model

First-party fraud — where a legitimate cardholder disputes a transaction they actually authorised — has become the defining challenge in chargeback management. According to Sift's Q4 2025 Digital Trust Index, first-party fraud represented 36% of all reported fraud in 2024, up from just 15% the year before, and forecasts project a 40% rise in such cases by 2026.

The reason this matters analytically is that friendly fraud cannot be detected or countered the same way third-party fraud can. The transaction is legitimate. The customer is real. Your fraud scoring tools gave it a clean bill of health. The dispute arrives weeks later, often coded simply as "unauthorised" because issuers default to that category when no clearer option exists.

Building analytics for friendly fraud requires a fundamentally different model. You need to construct a customer-level dispute history that joins across your CRM, your order management system, and your chargeback data — looking at patterns like:

- Repeat disputors: customers who have filed multiple chargebacks across a defined period

- Delivery confirmation vs. dispute: orders where carrier confirmation of delivery exists but a "not received" dispute was filed

- High-value, high-return-rate cohorts: customers whose combined refund, return, and dispute behaviour points to systematic abuse rather than genuine grievance

- Time-to-dispute distribution: friendly fraud typically arrives with a different lag pattern from genuine fraud, which tends to cluster in the first 0–7 days post-transaction

This kind of modelling lives in dbt. It requires stable customer identifiers, clean joins between order and payment data, and a semantic layer that makes these definitions consistent across every downstream report and alert. Without that infrastructure, your fraud team is left with gut feel and individual case review.

This directly connects to the broader point about fraud analytics for fintech operations — the same data foundations that power false-positive reduction also underpin your friendly fraud detection capability.

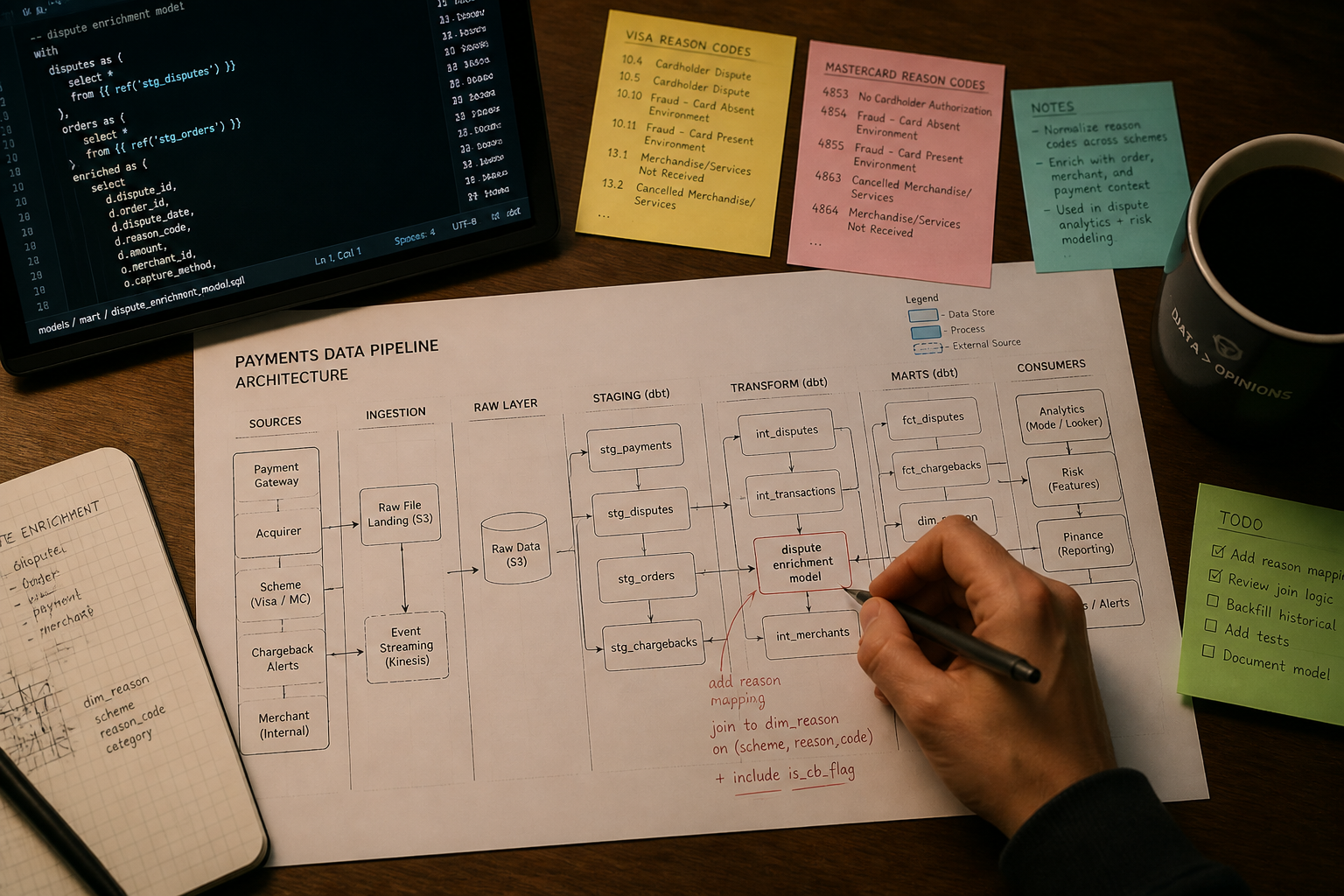

How to Structure Your Chargeback Analytics Data Stack

The architecture does not need to be complex to be effective. Here is the pattern we implement most often for Series A and Series B payments businesses:

Ingestion layer — Fivetran or a custom connector pulls dispute data from PSP APIs (Stripe, Adyen, Braintree, and most major acquirers expose webhook or REST endpoints). Order and customer data flows from your core platform. Fraud signals come from your risk tooling. Everything lands in BigQuery or AWS Redshift, depending on your existing stack.

Transformation layer (dbt) — This is where the analytical value is built. Core models include:

stg_disputes — normalised staging model, one row per dispute event

stg_orders — clean order data with stable transaction references

int_dispute_enriched — disputes joined to orders, customers, fraud scores, and delivery confirmation

mart_chargeback_performance — your production reporting model, pre-aggregated by reason code, merchant, time period, and dispute status

mart_friendly_fraud_signals — customer-level abuse indicators, refreshed daily

Migrating these calculations from spreadsheets into dbt models eliminates a class of recurring manual errors and cuts weekly maintenance time significantly — a result we have seen consistently across clients who made this transition.

Semantic layer — Holistics BI or Looker sits on top of these mart models, with metrics defined once and reused across all dispute reports. Chargeback rate, win rate, recapture rate, and dispute value by segment all live as governed, documented metrics. Finance, operations, and the fraud team are looking at the same numbers from the same definitions.

Alerting — dbt or a lightweight scheduler monitors key thresholds daily: spikes in reason code volume, merchants approaching VAMP risk territory, pre-dispute alert coverage dropping below target. An automated alerting system of this kind gives your payments operations team real-time visibility into dispute risk for the first time — reducing funding exposure and giving leadership a quantifiable measure of loss management performance.

A practical example: a reconciliation process at a payments company we worked with that previously took 30–50 minutes to run manually was rebuilt as an automated SQL pipeline. It now completes in under three seconds. The same principle applies to dispute reporting — what currently takes a finance analyst 90 minutes every Monday morning should be a live dashboard updated on every new data load.

The VAMP Threshold Change Has Raised the Stakes Materially

Visa's Acquirer Monitoring Programme (VAMP) reduced its threshold for the "excessive" chargeback designation to 0.9% from January 2026 (down from 1.5% in late 2025), with a $10 per disputed transaction fee applied to merchants above the limit. For any business processing at volume, this is a material change.

The implication is not just financial. Merchants who breach VAMP thresholds face heightened scrutiny from their acquirer, potential forced migration to a higher-cost pricing tier, and in persistent cases, termination of their merchant account. For a Series A payments platform with a single acquiring relationship, that is an existential risk.

Analytics has a direct role here. You need:

- A live VAMP ratio tracker — your current dispute count divided by eligible transaction count, updated daily, with a forward-looking projection based on the last 30 days of dispute arrivals

- Breach probability modelling — at your current trajectory, what is the probability of crossing 0.9% in the next 30, 60, and 90 days?

- Merchant-level risk segmentation — which merchants in your portfolio are contributing disproportionately to your aggregate ratio, and what is your contractual and operational response?

This kind of dashboard does not require sophisticated machine learning. It requires clean data, well-defined metrics, and a BI layer that surfaces the right information to the right people before the threshold is breached — not after.

For payments businesses operating across multiple corridors and acquiring relationships, the same architecture also underpins your broader cross-border payments analytics capability — dispute rates often vary significantly by corridor, and that visibility matters both operationally and commercially.

Frequently Asked Questions

Q: What is chargeback dispute analytics?

A: Chargeback dispute analytics is the practice of building structured data pipelines, dashboards, and models around your dispute lifecycle — covering reason code analysis, win rate tracking, recapture measurement, and friendly fraud detection. It transforms chargeback management from a reactive manual process into a governed, data-driven operation.

Q: How do I calculate my chargeback rate for VAMP compliance?

A: Your VAMP ratio is calculated as the number of disputes received in a given month divided by the total number of transactions processed in that same month. From January 2026, Visa's VAMP "excessive" threshold is 0.9%. You should be tracking this daily, not monthly, with a forward-looking projection to identify breach risk early.

Q: What chargeback metrics should I track beyond overall rate?

A: The most actionable metrics are chargeback rate by reason code, representment win rate by dispute category, pre-dispute alert coverage, dispute value concentration by merchant or SKU, and net recapture rate. These metrics identify where to intervene — the overall rate only tells you something has gone wrong.

Q: How do I detect friendly fraud in my chargeback data?

A: Friendly fraud detection requires joining your chargeback data to customer order history, delivery confirmation, and dispute frequency. Key signals include repeat disputors, "not received" disputes where delivery was confirmed, and time-to-dispute patterns that differ from genuine fraud. This modelling works best in a dbt layer where customer-level signals can be built and refreshed systematically.

Q: What data infrastructure do I need for chargeback dispute analytics?

A: At minimum, you need automated ingestion of PSP dispute data into a cloud data warehouse (BigQuery or Redshift), transformation models in dbt that join disputes to orders and customer data with normalised reason codes, and a BI layer (Holistics, Looker) that serves governed metrics to finance and operations teams. Manual CSV exports and spreadsheet models introduce errors and cannot scale.

Chargebacks are one of those areas where the gap between what fast-growing payments businesses know about their dispute exposure and what is actually happening in their data is consistently shocking — and consistently fixable. At Fintel Analytics, we have helped fintech startups, payments platforms, and e-commerce businesses build the data infrastructure that turns chargeback management from a Monday-morning spreadsheet exercise into a live, automated, decision-ready system. If your team is currently absorbing dispute losses without visibility into root cause, win rate, or breach risk, that is a solvable problem — and solving it pays for itself quickly.