Fraud Analytics for Fintech Payments: How to Fix Your False Positive Problem

Fraud analytics for fintech payments is the discipline of building data infrastructure, ML models, and monitoring pipelines that detect fraudulent transactions while minimising the number of legitimate payments incorrectly declined. Done well, it protects revenue on both sides of the ledger — from actual fraud losses and from the conversion damage caused by false positives. Done poorly, it becomes one of the most expensive data problems a payments business can have.

Most early-stage fintechs do not have a fraud detection problem. They have a fraud data problem. The model is a secondary concern; the infrastructure that feeds it — event logging, feature engineering, labelling pipelines, and monitoring — is where deals are won and lost. And based on what we see working with payments companies across the UK, Europe, and APAC, most teams are sitting on bad infrastructure and blaming the model.

Why False Positives Are Now the Bigger Business Risk

The instinct when building fraud controls is to tighten thresholds — catch more fraud, minimise losses. The problem is that tightening rules-based controls without robust analytics infrastructure behind them creates a different, often larger, problem: blocking customers who were going to pay.

The numbers on this have become alarming. According to Fraudio's 2026 tracking data, the global false-positive proxy for payment declines has nearly doubled over five years, reaching 23.5% in May 2026. That means roughly one in four transaction declines is blocking a legitimate, revenue-generating customer. In traditional e-commerce channels specifically, false-positive rates have been recorded at over 23.7%.

This is not a model accuracy problem in isolation. It is a data architecture problem. Rules-based fraud systems — velocity limits, static IP blocks, rigid BIN-level rules — are inherently unable to distinguish a genuine customer from a fraudster using the same channel, device type, or geography. The underlying data simply is not rich enough, and there is no feedback loop to learn from errors.

Meanwhile, the fraud threat itself is escalating. Financial crime generated $579.4 billion in global losses in 2025, according to the Nasdaq Verafin Global Financial Crime Report — a figure recorded across a year in which 67% of banks and fintechs reported rising fraud rates. Fraud rates across payments networks climbed from 0.036% in 2024 to 0.045% across the 2025–2026 period. The pressure on fraud teams is real. But overcorrecting with blunt controls is just trading one loss for another.

At Fintel Analytics, a pattern we see repeatedly in early-stage fintech clients is the same sequence: the payment operations team triggers an incident response after a fraud spike, thresholds are tightened manually, and conversion drops by 3–8% over the following weeks without anyone correlating the two events. The fraud team and the product team are not looking at the same data.

📺 Watch: Fraud Detection with SQL 💳 | Catch Payment Scams in Real-Time!

What a Fraud Analytics Data Stack Actually Needs

The gap between a fraud team that is fighting fires and one that is systematically winning is almost always an infrastructure gap, not a talent gap. Here is what a properly engineered fraud analytics stack looks like at Series A to Series B scale.

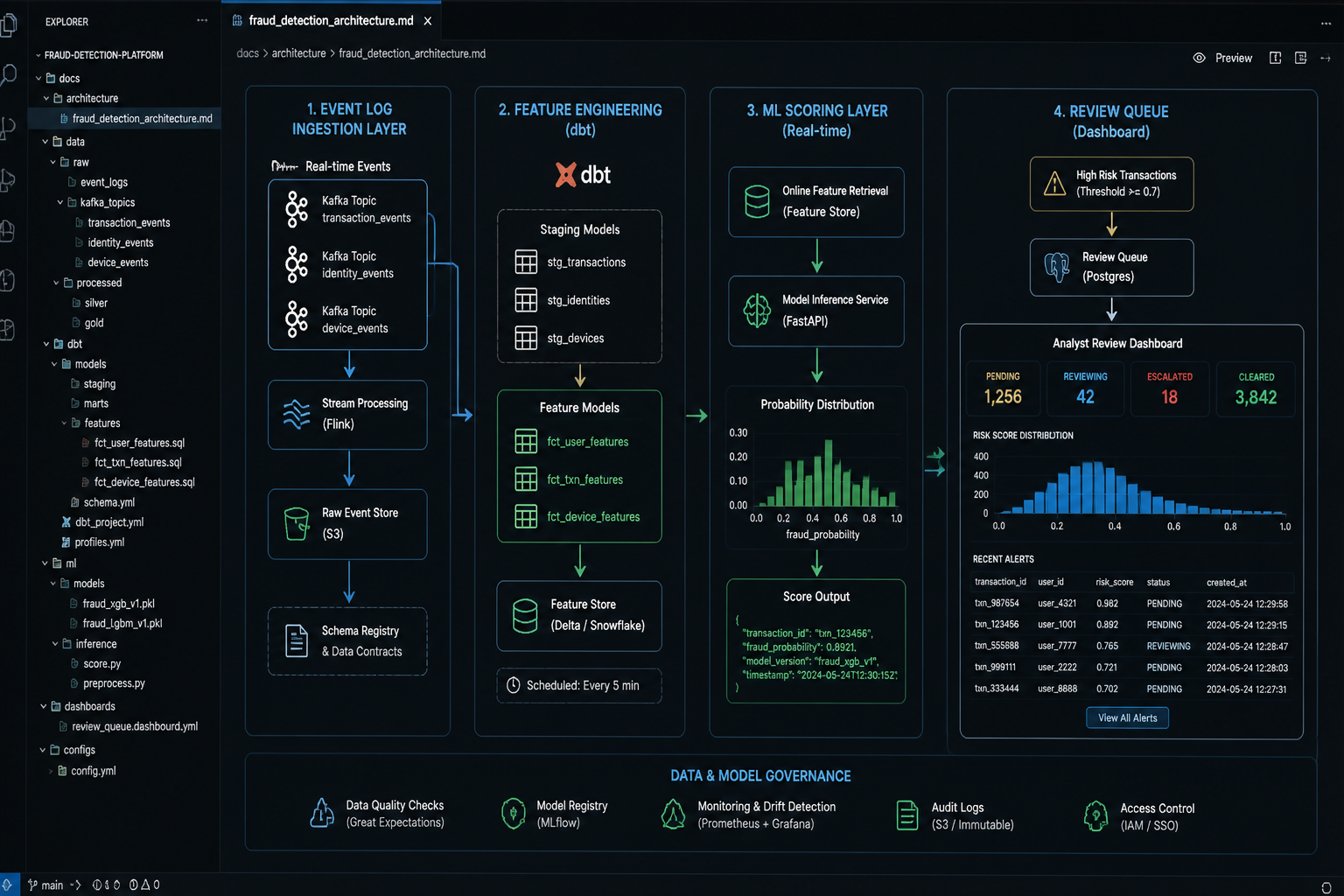

1. A Clean, Immutable Transaction Event Log

Everything starts here. Your fraud models are only as good as the event data feeding them. In practice, this means:

- Every payment event — attempt, authorisation, decline, chargeback, refund — logged immutably with a consistent schema

- Device fingerprints, IP metadata, session identifiers, and merchant context captured at event time (not reconstructed later)

- Millisecond-resolution timestamps, critical for velocity feature construction

- No event loss — at the transaction volumes fintechs operate at, dropped events corrupt model training data in ways that are almost impossible to detect

A pattern we see regularly: raw event logs are stored in a flat table with no partitioning, queried by the data team using full scans, and the resulting feature store is being rebuilt from scratch every time someone wants to retrain the model. The engineering cost compounds quickly.

If you are at Series A scale and your transaction event table is a single BigQuery or Redshift table without partitioning, clustering, or incremental loading — you are already accruing technical debt that will become a model reliability problem within 12 months.

2. A Feature Engineering Pipeline That Survives Production

The majority of fraud model failures in production are not model failures — they are feature pipeline failures. Training-serving skew, where the features used to train the model are computed differently from the features served at inference time, is endemic in fintech fraud stacks built under pressure.

Practically, this means:

- All features used in the fraud model should be computed from the same SQL transformation logic, managed in a version-controlled dbt project

- Point-in-time correct feature computation — velocity windows (transactions in last 1/5/15/60 minutes), aggregated risk signals (average spend by device, merchant category exposure by card), and behavioural baselines must all be computed as of the event timestamp, not the training run timestamp

- A feature store with a read path fast enough for real-time inference (typically sub-100ms) and a write path that feeds the training dataset consistently

If you want to go deeper on the specific failure modes here, we have covered the mechanics of training-serving skew and how to fix it in our guide to ML feature pipelines for startups.

3. A Labelling Pipeline That Actually Reflects Reality

This is the part most fraud teams underinvest in, and it is where model quality degrades quietly over time.

Fraud labels arrive late — chargebacks can take 60–90 days to materialise. Models trained on near-real-time data therefore train on incomplete labels, systematically underestimating fraud rates in recent cohorts. Without a delayed label reconciliation pipeline, every model retraining run is producing a model that is slightly miscalibrated toward the recent past.

A properly designed labelling pipeline:

- Stages transactions with provisional labels at T+0 and updates them as chargebacks, disputes, and manual review outcomes arrive

- Maintains a historical label log so training datasets can be reconstructed with labels as they were known at any given point in time

- Flags the proportion of the training window that has incomplete labels — surfacing this to the model owner as a data quality signal, not hiding it

How to Measure Whether Your Fraud Analytics Stack Is Working

Most fraud teams track fraud loss rate. Fewer track the metrics that capture the full economic picture. Here is the framework we use when auditing a client's fraud analytics setup:

Fraud loss rate — fraudulent transaction value as a percentage of total processed volume. The metric everyone watches.

False positive rate (FPR) — legitimate transactions declined as a percentage of all declined transactions. The metric that ties directly to revenue leakage. At institutional transaction volumes, the analyst workload and conversion damage generated by a 5–8% false positive rate becomes a primary operational cost, often exceeding the losses it was designed to prevent.

Chargeback-to-transaction ratio — chargebacks as a percentage of total transactions. A lagging indicator, but important for PSP relationship health and scheme compliance thresholds.

Review rate — what percentage of transactions are being routed to manual review, and what is the outcome distribution? A high review rate with a low conversion-to-fraud-confirmed rate is a signal that your model is not discriminating well.

Model degradation rate — how quickly does precision and recall decay between retraining cycles? If you are not measuring this in production, you will not know your model has degraded until you see it in the fraud loss rate — which is a 30–60 day lag.

If you are in the market for how to instrument model degradation tracking in production, our guide to ML model monitoring for startups covers the specific metrics and tooling we deploy for clients.

If you are looking to build or audit this kind of fraud analytics infrastructure in your business, explore how Fintel Analytics approaches this — we work with payments businesses and fintechs globally to design and deliver exactly this kind of solution, from event pipeline design through to model monitoring in production.

The Architecture Decision: Rules Engine, ML Model, or Both?

This is the most common strategic question we get from payments CTOs in the Series A to Series B window. The honest answer is: both, in sequence, with explicit handoffs.

Rules engines are fast to deploy, transparent, and auditable. They are appropriate for catching high-confidence fraud signals — known bad IP ranges, velocity patterns that no legitimate customer would generate, BIN combinations associated with confirmed compromised card data. They are inappropriate as the primary mechanism for nuanced scoring decisions, because they cannot generalise to new fraud patterns and they generate false positives at scale.

ML models — gradient boosting, neural networks, ensemble methods — are appropriate for the probabilistic scoring layer. They generalise better, adapt to new patterns (with retraining), and can incorporate hundreds of features simultaneously. Their weaknesses: they require good training data, they degrade in production, and they are harder to explain to regulators and to your risk committee.

The architecture we typically deploy for Series A fintechs:

- Pre-filter rules layer — synchronous, high-confidence hard blocks (sub-5ms)

- ML scoring layer — asynchronous probabilistic score returned within 100–200ms, informing the approve/review/decline decision

- Post-transaction review layer — a human review queue, fed by the model's "uncertain" zone (typically 0.3–0.7 probability range), with outcomes fed back into the labelling pipeline

- Monitoring layer — daily model performance metrics, automated alerts on FPR drift, precision/recall degradation, and distribution shift in incoming features

The combination of AI detection with rich data infrastructure is proving decisive. In 2025, Mastercard reported that embedding generative AI across its fraud detection systems delivered up to a 300% improvement in detection rates — but that result is only achievable when the underlying data infrastructure is solid enough to feed the model cleanly.

Real-World Outcomes: What Good Fraud Analytics Delivers

To ground this in delivery experience:

A Series A payments company we worked with had a rules-based fraud system that was generating a false positive rate well above industry norms. The root cause was not the rules themselves — it was that the velocity features underpinning the rules were being computed over a rolling window that was incorrectly anchored, producing inflated velocity counts for customers on shared IP infrastructure (mobile carrier NAT, VPNs). Legitimate customers were being declined at rates that were visibly damaging conversion in their top three corridors.

The fix involved rebuilding the feature pipeline in dbt with correctly scoped window functions, revalidating the velocity logic against a 90-day historical dataset, and recalibrating the rule thresholds using the corrected feature distributions. The false positive rate dropped materially within two billing cycles, and the operations team had a dashboard — built in Holistics — that surfaced FPR by corridor, device type, and time of day for the first time.

Separately, in a reconciliation and fraud audit project for a global fintech, the process of building a proper transaction event model in BigQuery uncovered a $25M discrepancy that had gone undetected in the existing reporting. At market borrowing rates, that gap was costing over $6,000 per day.

The common thread: the model was never the problem. The data was.

Frequently Asked Questions

Q: What is fraud analytics for fintech payments?

A: Fraud analytics for fintech payments is the combination of data engineering, feature pipelines, ML modelling, and monitoring infrastructure that enables a fintech to detect fraudulent transactions in real time while minimising false positives — legitimate transactions incorrectly declined. It encompasses the full stack from raw event logging through to model scoring, review workflows, and production monitoring.

Q: What causes a high false positive rate in payments fraud detection?

A: High false positive rates are most commonly caused by overly rigid rules-based systems, poorly engineered velocity features, and the absence of a feedback loop that updates the model on the outcomes of declined transactions. Rules calibrated on historical fraud patterns fail to distinguish legitimate customers who share surface-level characteristics — IP ranges, geographies, device types — with known fraudsters.

Q: What data does a fraud detection ML model need to work well?

A: A fraud ML model requires a clean, immutable transaction event log with millisecond timestamps; point-in-time correct features including velocity windows, behavioural baselines, and device signals; and a delayed label reconciliation pipeline that updates fraud labels as chargebacks and disputes materialise. Without all three, the model will either degrade in production or be miscalibrated from the first training run.

Q: How do you measure the performance of a fraud analytics system?

A: Beyond fraud loss rate, a well-instrumented fraud stack tracks false positive rate (legitimate declines as a percentage of all declines), review rate and review outcome distribution, chargeback-to-transaction ratio, and model degradation rate between retraining cycles. Tracking only fraud loss rate is a lagging signal that hides conversion damage caused by false positives.

Q: When should a fintech startup invest in a proper fraud analytics stack?

A: The trigger is typically when rules-based controls start producing visible false positive rates above 5%, when chargeback ratios approach scheme thresholds, or when the fraud team is spending more time in spreadsheets than in a structured review workflow. At Series A scale and above, ad-hoc rules management becomes a liability — both operationally and in terms of the model quality you can sustain.

Fraud analytics for fintech payments is one of the highest-stakes data engineering problems a growth-stage company faces — getting it wrong costs revenue on both sides of the ledger, and the failure is often invisible until it shows up in a chargeback dispute or a conversion drop that nobody can explain. At Fintel Analytics, we have helped payments businesses and fintechs build the event pipelines, feature stores, and monitoring infrastructure that make fraud models reliable in production — not just in a Jupyter notebook. If your fraud stack is running on rigid rules, manual thresholds, and a spreadsheet for reviewing declines, that is a solvable problem, and solving it pays for itself faster than almost any other data investment you will make.