Neobank Analytics: Build the Data Stack That Scales in 2026

A neobank analytics data stack is the combination of data pipelines, warehousing, transformation models, and BI tooling that turns raw transaction, product, and customer data into the metrics that drive commercial decisions. Without one, fast-growing neobanks fly blind — scaling user numbers while remaining unable to answer basic questions about profitability, activation, or risk. In a sector where over 76% of neobanks remain unprofitable in 2026, the difference between the businesses that survive and those that don't often comes down to how well they understand their own numbers.

The neobank market is enormous and accelerating. The neobanking market has grown exponentially in recent years, projected to grow from $261.4 billion in 2025 to $385.05 billion in 2026 at a CAGR of 47.3%. Worldwide, neobank users are expected to hit 350 million in 2026. But scale and profitability are very different things. A pattern we see repeatedly is neobanks that have grown to 200,000 users and still cannot tell you definitively what their cost-to-serve per active user is, or which product cohorts are actually contributing margin. The data exists — spread across a core banking system, a BaaS provider, a card processor, a KYC vendor, and a CRM — but nothing connects it into a coherent picture.

This post is for the CTO, Head of Product, or CFO at a growth-stage neobank who knows the numbers are broken and is trying to figure out where to start fixing them.

Why Neobank Data Is Harder to Unify Than Most Fintech Verticals

Neobanks are rarely built on a single system. Many neobanks operate without standalone banking licences and must partner with existing financial institutions, relying on multiple banking-as-a-service (BaaS) providers to deliver their offerings. That operating model is commercially sensible — but it creates a data fragmentation problem from day one.

A typical early-stage neobank might be pulling data from:

- A core banking or ledger provider (e.g. Mambu, Thought Machine, or a proprietary ledger)

- One or more BaaS partners for account infrastructure

- A card processing network for interchange and authorisation data

- A KYC/AML vendor for onboarding event data

- A mobile analytics tool for in-app behavioural events

- A CRM or support platform for customer lifecycle data

- An internal PostgreSQL or MySQL operational database for product state

Each of these systems uses different identifiers, different event schemas, different timestamp conventions, and different definitions of what constitutes an "active" user or a "completed" transaction. When a product manager asks "how many users activated their card within 7 days of signing up?", the answer might require joining six different data sources — and without a properly engineered pipeline, the answer you get depends entirely on which source you queried last.

A modern neobank architecture in 2026 is digital-first, API-driven, and built on microservices over cloud-native infrastructure, following an outside-in approach where user experience shapes system design, with each layer decoupled via APIs. That's excellent for product velocity — but it creates an analytics environment where the data is distributed across a dozen microservice databases, none of which were designed with reporting in mind.

The fix is not to consolidate operational systems. The fix is to build an analytics layer that ingests, normalises, and models data from all of these sources into a single warehouse — and then build the metrics on top of it that the business actually needs.

📺 Watch: How to Build a Robust Neobank Core Banking System| 2026 Guide

The Five Metrics a Neobank Must Get Right Before Series B

Before we get into architecture, it's worth being concrete about what you're actually trying to measure. Investor scrutiny at Series A and B focuses tightly on a small number of unit economics questions, and these are the same metrics that should be driving your product decisions week to week.

1. Cost-to-Serve Per Active User This is not just your monthly burn divided by your user count. It should include an allocated share of BaaS fees, card processing costs, KYC costs, customer support load, and infrastructure — segmented by product line and user tier. Most neobanks we work with have never calculated this at a per-user level. Some are surprised to find they're losing money on their heaviest users.

2. Activation Rate and Time-to-Activation How many users who signed up completed their first transaction? In how many days? What's the dropout rate at each onboarding step? Product decisions for a neobank require interpretation of cohort behaviour, funnel breaks, payment success rates, KYC rejection reasons, and card activation patterns. These metrics only become visible when onboarding event data from your KYC vendor, your app, and your core banking system are stitched together in a single pipeline.

3. Monthly Active Users (MAU) — Properly Defined This sounds simple. It isn't. In our experience, neobank MAU figures are often inflated by users who logged in but didn't transact, or by test accounts that were never properly excluded. When the definition lives in a spreadsheet maintained by the growth team rather than in a versioned dbt model, it will drift — and you'll end up with different answers in different decks. The first time an investor asks for the underlying methodology and you can't show them a clean SQL model, you've got a credibility problem.

4. Net Revenue Per User Interchange, FX margin, premium subscription fees, interest income — how much is each user actually generating, net of directly attributable costs? This metric needs to be built from multiple source systems and is almost never correct the first time you try to calculate it. A common error is double-counting BaaS cashback incentives against interchange, or failing to account for currency conversion costs in multi-currency accounts.

5. Cohort Retention and LTV Which sign-up cohorts are still active at 30, 60, and 90 days? What's the LTV distribution across your customer segments? These questions require cohort tables built on top of clean transaction and event data — the kind of tables that only exist once you have a proper warehouse and transformation layer in place.

If even one of these five metrics is calculated differently by finance and product, or lives in a spreadsheet that a single analyst maintains, you have a data governance problem — and it will surface at the worst possible time.

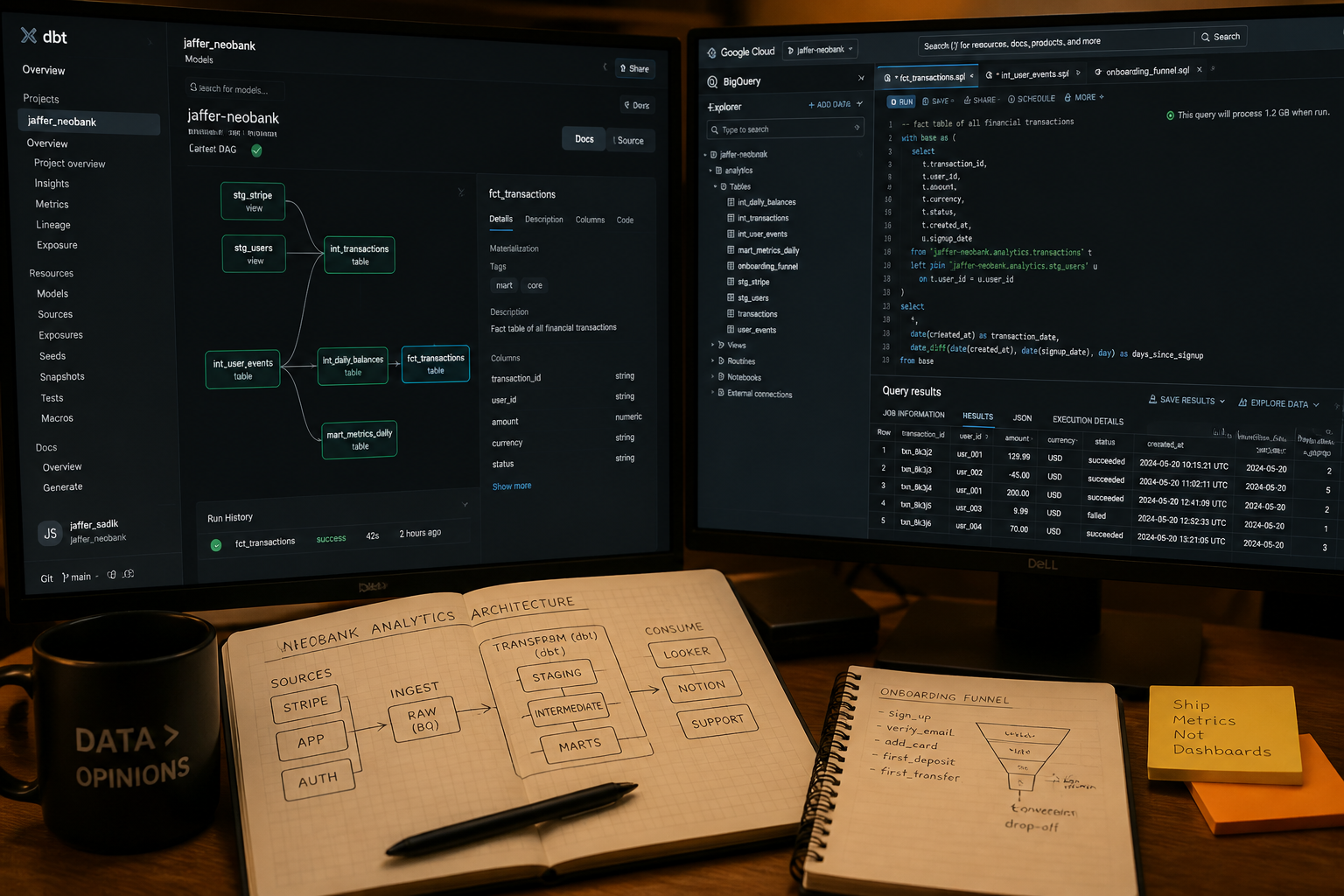

What the Neobank Analytics Stack Actually Looks Like

Here is the architecture we recommend — and have delivered — for growth-stage neobanks operating at pre-Series A through Series B scale.

Ingestion Layer All source systems — BaaS APIs, card processor webhooks, KYC event feeds, app analytics streams, and operational databases — feed into a cloud data warehouse. For most neobanks, BigQuery or AWS Redshift is the right choice at this scale. The ingestion mechanism depends on the source: most SaaS tools are handled by a managed connector (Fivetran or Airbyte); operational databases require CDC (change data capture) pipelines; real-time event streams require a Kafka or Pub/Sub layer for anything latency-sensitive.

Transformation Layer (dbt) Raw ingested data is never queried directly by dashboards or analysts. dbt models normalise source schemas, resolve identifier mismatches between systems, apply business logic (the definition of "active user", the calculation of net revenue), and produce clean mart tables that all downstream consumers draw from. Crucially, metric definitions live here — not in a spreadsheet, not in a BI tool formula, not in someone's head. When the definition of MAU changes (and it will), you change it in one dbt model and it propagates everywhere.

In our work with early-stage neobanks, migrating calculations out of Google Sheets and into dbt models eliminates an entire class of recurring errors. One client cut their weekly finance reporting preparation time by 30 minutes per week, just by moving three key metric calculations into tested SQL models.

Semantic Layer and BI Once your dbt models are in place, the semantic layer defines how metrics are calculated, labelled, and exposed to business users. We use Holistics BI for many of our neobank clients — it handles the semantic modelling, access control, and self-service reporting in a single tool that integrates cleanly with dbt and BigQuery. The alternative is Looker for teams that need deeper custom embedding or white-labelling. Either way, the principle is the same: one place where metric definitions live, one place where dashboards are built, and one version of the truth for the entire organisation.

Alerting and Monitoring For a neobank, certain data conditions need to trigger an alert rather than wait for a morning dashboard review — a spike in failed card transactions, a KYC rejection rate above threshold, or a sudden drop in daily active users. These operational alerts should be built as part of the analytics layer, not left to the engineering team's monitoring tooling, which typically covers infrastructure health but not business metrics.

An automated alerting system gives a treasury and operations team real-time visibility into risk conditions for the first time — reducing funding misses and giving leadership a quantifiable measure of operational health.

If you're looking to design and build this stack for your neobank, explore how Fintel Analytics approaches this — we work with growth-stage fintech businesses globally to design and deliver exactly this kind of data infrastructure.

The Three Mistakes Neobanks Make When Building Their Analytics Stack

Mistake 1: Reporting on raw transactional data without normalisation The most common error we see is a neobank that has connected their data warehouse directly to their BI tool and pointed analysts at raw transaction tables. The result: every dashboard query re-implements the same business logic inconsistently, metrics drift, and the same number comes out differently in three different places. Neobanks now operate at the intersection of embedded finance, advanced data analytics, and API-driven partnerships — which means the raw data is inherently complex. You cannot skip the transformation layer and expect accurate reporting.

Mistake 2: Treating the analytics stack as an engineering project rather than a product Data infrastructure built by engineers for engineers tends to be technically correct but commercially useless. We've seen neobanks with beautifully constructed Kafka pipelines and no dashboard that answers "what is our card activation rate this week?" The analytics stack needs to be driven by the business questions — start with the five metrics above, build the models that produce them, and then work backwards to the ingestion architecture you need.

Mistake 3: Underestimating the cost of bad data A capital reconciliation error that goes undetected for weeks is not a theoretical risk — it's a lived experience for many neobanks operating across multiple BaaS providers and settlement cycles. In one project we delivered for a global fintech, a reconciliation process that took 30–50 minutes to run was rebuilt as an automated SQL pipeline that now completes in under 3 seconds. The speed improvement was significant. But the more important finding was the $25M discrepancy that the automated reconciliation surfaced — one that had gone undetected under the previous manual process. At market borrowing rates, that gap was costing over $6,000 per day.

For more detail on how analytics applies specifically to reconciliation at scale, see our piece on Payments Reconciliation Analytics: Automate & Scale in 2026. And if your neobank is building out interchange and BaaS cost tracking, the principles in Interchange Fee Analytics: Stop Flying Blind on Card Costs are directly applicable.

When Should a Neobank Invest in Analytics Infrastructure?

This is the question founders most often get wrong — and the answer is almost always "earlier than you think".

The temptation is to defer the analytics investment until after product-market fit, after the Series A, after you've "got enough data to make it worthwhile". But in our experience, the neobanks that come to us post-Series A with a broken data stack have already made three years of product decisions on bad numbers. They've optimised their onboarding flow based on activation metrics that were double-counting users. They've reported MAU to investors using a definition that changes every quarter. They've built their unit economics model in Excel and had it diverge from reality by the time they reached 50,000 users.

The right moment to invest in analytics infrastructure is when:

- You have more than two source systems contributing to your core metrics

- You have more than one person asking data questions regularly

- You are preparing for investor reporting or a fundraise

- You've noticed that finance and product are reporting different numbers for the same metric

For most neobanks, that moment arrives somewhere between 10,000 and 50,000 users — well before Series A. The cost of building it right at that stage is far lower than the cost of fixing it after two years of technical debt have accumulated.

The investment pays for itself quickly. Weekly executive reporting that previously required 90 minutes of manual preparation can be replaced by a live dashboard — zero manual effort, updated hourly — within weeks of deployment. That's not a future-state aspiration; it's a repeatable outcome we deliver for clients regularly.

Frequently Asked Questions

Q: What data does a neobank analytics stack need to ingest?

A: A complete neobank analytics stack should ingest data from all core operational systems: the core banking or ledger platform, BaaS partner APIs, card processor transaction and authorisation feeds, KYC/AML event data, mobile app behavioural events, CRM data, and any internal operational databases. The goal is a single warehouse where all of these sources are unified under consistent identifiers and schemas.

Q: What is the best data warehouse for a neobank at Series A scale?

A: BigQuery is the most common choice for growth-stage neobanks due to its serverless architecture, cost-effective pricing at moderate data volumes, and excellent integration with dbt and modern BI tools. AWS Redshift is a strong alternative for teams already running on AWS infrastructure. The choice matters less than ensuring the transformation and semantic layers above it are properly built.

Q: How does dbt fit into a neobank analytics stack?

A: dbt (data build tool) sits in the transformation layer of the stack. It takes raw data from your warehouse and applies business logic — normalising schemas, resolving identifier mismatches across source systems, defining metric calculations, and producing clean mart tables for dashboards and analysis. For a neobank, dbt is particularly valuable because it allows metric definitions (MAU, activation rate, net revenue per user) to be version-controlled, tested, and maintained in one place rather than scattered across spreadsheets and BI tool formulas.

Q: How should a neobank define Monthly Active Users (MAU) in their data model?

A: MAU should be defined in a dbt model, not a spreadsheet or dashboard formula. The definition should explicitly exclude: test and internal accounts, users who logged in but performed no transaction or meaningful product interaction, and duplicate user records from your onboarding system. The exact definition will vary by product — some neobanks define activity as a card transaction, others include P2P transfers or savings deposits — but it must be codified, documented, and consistent across all reporting surfaces.

Q: What BI tool should a neobank use for product and finance reporting?

A: For most growth-stage neobanks, a semantic-layer-first BI tool is the right choice — one where metric definitions are centralised and self-service reporting is accessible to non-technical stakeholders. Holistics BI is well-suited for teams using BigQuery and dbt, with clean semantic modelling and strong access control. Looker is a strong alternative for teams needing deeper embedding or more complex custom dashboards. Avoid tools where metric logic lives inside the BI layer itself — that recreates the same fragmentation problem you're trying to solve.

Neobanks that reach Series B with a robust analytics stack are in a fundamentally different position to those that arrive with five competing spreadsheets and a BI tool nobody trusts. At Fintel Analytics, we have built production data infrastructure for growth-stage fintech businesses across payments, digital banking, and embedded finance — from initial architecture design through to deployed dashboards and automated pipelines. If your team is making critical product and financial decisions without a single source of truth underneath them, that is a solvable problem — and solving it now is significantly cheaper than solving it under the pressure of a fundraise or a regulatory review.