Financial close analytics is the practice of replacing manual spreadsheet-based close processes with automated data pipelines, governed SQL models, and live BI dashboards — so finance teams produce accurate numbers faster, with less human intervention. Done properly, it compresses a five-to-ten-day close cycle into one to three days while eliminating the class of errors that come from copying figures between systems.

If your finance team is still spending the first week of every month chasing numbers across ERP exports, payment processor reports, and shared Google Sheets, you are not facing a process problem. You are facing a data infrastructure problem. And it has a concrete fix.

Why Is the Month-End Close Still So Painful in 2026?

The uncomfortable answer is that most growth-stage companies have built their financial reporting stack on tools that were never designed for the volume or complexity they now operate at. When a company is doing a few thousand transactions a month, reconciling in Excel is tolerable. When it is doing tens of millions — across multiple payment providers, currencies, entities, and cost centres — the spreadsheet breaks under its own weight.

The numbers are stark. A 2025 Forbes Finance Council analysis found that 50% of finance teams require six or more days for month-end work — equivalent to 140+ hours of repetitive accounting per close cycle. Only 18% of teams close in three days or fewer, while half still take longer than a week.

What drives that delay is rarely the final reporting step. It is everything that happens before: reconciling fragmented data, aligning upstream systems, and correcting manual errors. The reconciliation of bank accounts, payment processors, and internal ledgers consistently tops the list of time-consuming close activities — not because it is intellectually hard, but because the data pipelines feeding it are unreliable.

A pattern we see repeatedly at Fintel Analytics: a Series A fintech with three payment providers, two banking rails, and a Stripe integration is trying to reconcile its ledger from six different CSV exports, each with different timestamp formats, currency handling, and fee structures. Someone on the finance team owns a master spreadsheet. When they are on holiday, the close does not happen. That is not a staffing problem. It is an architecture problem.

📺 Watch: Understanding the Financial Closing Process

What Does a Broken Financial Close Data Stack Actually Look Like?

Before building a solution, it helps to name the failure modes precisely — because the symptoms look different depending on which part of the stack is broken.

Upstream data quality failures. Raw transaction files from PSPs, banks, and ERP systems arrive in inconsistent formats. Fee structures differ between providers. Refunds and chargebacks hit in a different period than the original transaction. When these are reconciled manually, errors accumulate silently. Businesses implementing automated reconciliation systems see a dramatic 70% reduction in data entry errors during month-end close processes. The inverse of that statistic is that manual processes carry a structural error rate that compounds month over month.

No single source of truth. Finance uses one export, operations uses another, leadership sees a third figure from a dashboard built on stale data. The same metric — revenue, fees paid, net settlement — shows three different numbers depending on who you ask. In our experience, this is not a governance failure so much as an infrastructure failure: there is no agreed-upon layer where metrics are defined, versioned, and shared.

Manual transformation in spreadsheets. The most dangerous part of most financial close stacks is not the ERP — it is the Excel or Google Sheets file that sits between the ERP and the board pack. Calculations live in cell references that nobody has documented. One deleted row breaks a formula that nobody notices until the numbers do not add up at the next audit. Globally, 2.5 million finance professionals rely on Excel for 70% of daily tasks (IDC, 2024), and while that reflects Excel's genuine utility, it also describes a widespread single point of failure in financial reporting.

No orchestration or monitoring. Pipelines run manually or on fragile scheduled scripts. There is no alerting when a source file does not arrive, when a reconciliation breaks, or when volumes look anomalous. The first sign that something went wrong is often a number that looks wrong in the board pack — by which point it is too late to investigate calmly.

How Do You Build a Financial Close Analytics Stack That Actually Works?

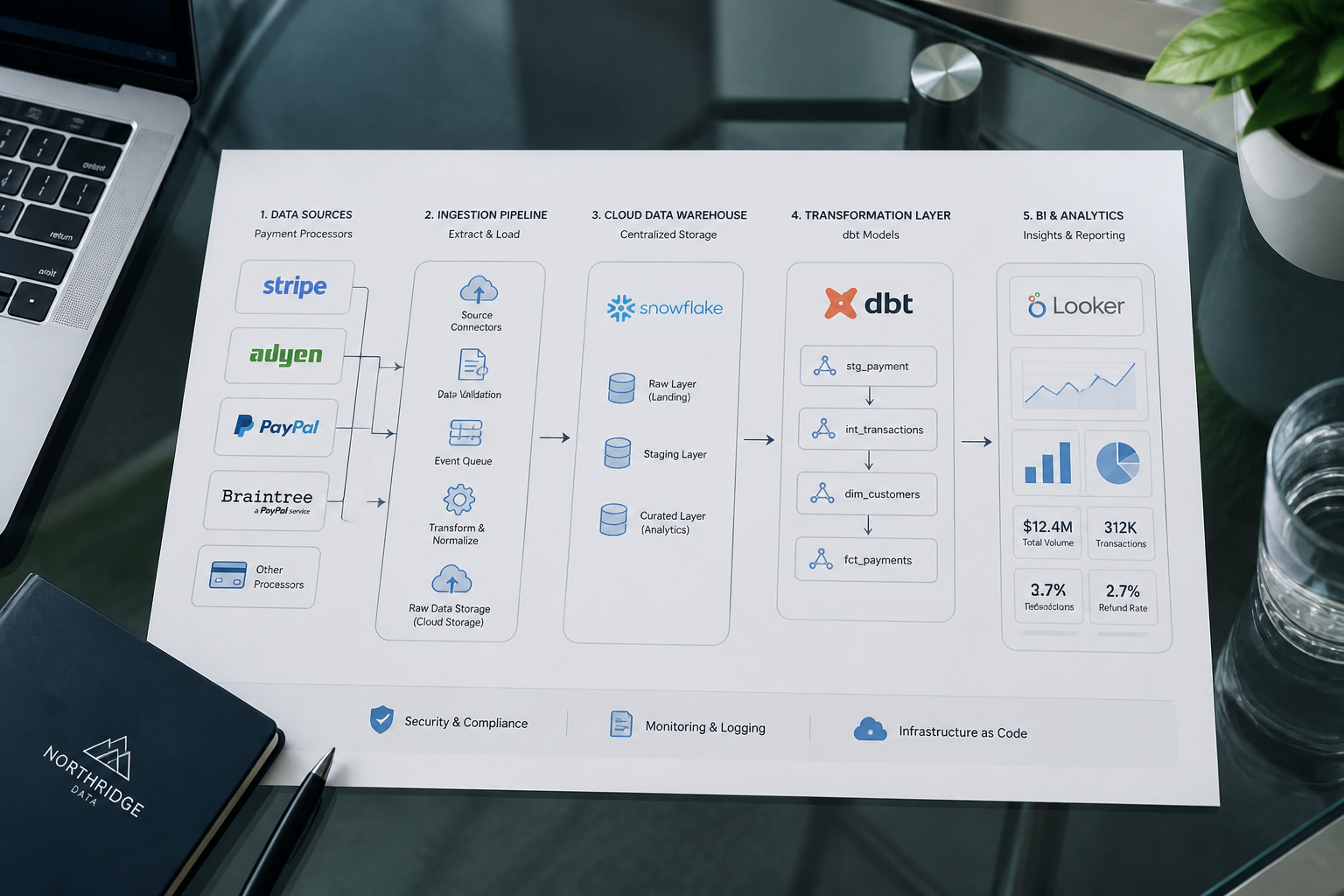

The architecture for a modern financial close analytics stack follows a clear pattern. The components are not exotic — BigQuery or a comparable cloud warehouse, dbt for transformation and modelling, an orchestration layer, and a BI tool for final presentation. What matters is how they are wired together and what discipline is applied at each layer.

Step 1 — Standardise your ingestion layer. Every source system — payment processors, banking APIs, ERP exports — should feed into a raw data layer with a consistent schema. This means writing ingestion pipelines that handle format normalisation upstream, before any business logic is applied. Timestamps in UTC. Amounts in a base currency with original currency preserved. Transaction statuses mapped to a controlled vocabulary. This is unglamorous work, but it is the foundation everything else depends on.

Step 2 — Model your reconciliation logic in dbt. The reconciliation rules that currently live in spreadsheet formulas belong in SQL models — versioned, tested, and documented. A dbt model that matches PSP settlements to bank credits, flags discrepancies above a threshold, and produces a clean reconciliation output is auditable, repeatable, and maintainable by anyone on the team. When the rules change — a new fee structure, a new provider — the change is made in one place and propagates everywhere.

We have delivered exactly this kind of transformation for clients in the payments space. A reconciliation process that took 30–50 minutes to run manually was rebuilt as an automated SQL pipeline — it now completes in under 3 seconds. That is not just a speed improvement; it means the reconciliation can run continuously throughout the month, surfacing discrepancies in near real-time rather than at period end.

Step 3 — Define your financial metrics in a semantic layer. Revenue, gross margin, fees as a percentage of volume, net settlement — these should be defined once, in a semantic layer, and referenced everywhere. If finance and the board are looking at the same dashboard fed by the same SQL model, they cannot see different numbers. The metric is the metric. If you want to understand the broader case for this approach, our post on SQL Semantic Layer: Why Your Metrics Are Broken in 2026 covers the architecture in detail.

Step 4 — Orchestrate and monitor everything. Every pipeline should be scheduled, monitored, and alerting on failure. A missing file from a PSP should trigger an alert before it becomes a close delay. Volume anomalies — a day with zero transactions, an unexpected spike in fees — should surface automatically. The finance team should never discover a data problem during the close; they should have been told about it days earlier.

Step 5 — Build close dashboards that replace the manual board pack. The output of this stack is a set of live dashboards that finance and leadership can access at any time, showing figures they trust. No manual compilation. No "here is the latest version" email. Companies using integrated systems report 87% faster access to financial information compared to those using separate platforms (2024 data). The close dashboard should show reconciliation status, outstanding items, period-to-date P&L, and cash position — all from the same underlying models.

If you are looking to implement this kind of stack in your organisation, explore how Fintel Analytics approaches financial data engineering — we work with fintech, payments, and e-commerce businesses globally to design and deliver exactly this kind of solution.

What Does This Actually Cost to Build, and What Does It Save?

The ROI question is always legitimate, so let us answer it directly.

The build cost for a well-scoped financial close analytics stack at a Series A or B company typically involves a few weeks of data engineering work: ingestion pipelines, dbt models for core reconciliation logic, a semantic layer for financial metrics, and a BI layer on top. The ongoing maintenance overhead is low — a small number of models to update when source schemas change, pipeline monitoring to handle.

The savings side of the equation is more interesting. Consider the time cost first. If five people across finance, operations, and leadership each spend ten hours per close cycle on manual data gathering, reconciliation, and report compilation, that is 50 person-hours per month — 600 per year. At a blended cost of £60 per hour, that is £36,000 annually in labour alone, before you account for the opportunity cost of a CFO spending close week in spreadsheets rather than advising on strategy.

Then there is the error cost. Studies show that companies implementing AI-powered reconciliation solutions experience 85% faster reconciliations compared to manual methods. More critically, the errors that manual reconciliation misses can be materially expensive. In our work with a fintech client, a capital reconciliation project uncovered a $25M discrepancy that had gone undetected — at market borrowing rates, that gap was costing over $6,000 per day. No spreadsheet-based process had flagged it. An automated pipeline with variance alerting would have surfaced it within 24 hours of it appearing.

Companies report cutting their close time from 7 days to 2–3 days after implementing month-end close automation tools. For a growth-stage business preparing for a Series B, a fundraise, or an audit, the ability to produce accurate financials quickly is not just an operational nicety — it is a commercial asset.

What Are the Most Common Mistakes When Automating the Financial Close?

Based on delivery experience, the mistakes that derail financial close analytics projects tend to cluster around a few predictable failure points.

Automating a broken process. If your current reconciliation logic is wrong — if there are known edge cases handled inconsistently in different versions of the spreadsheet — automating it codifies the errors. The first step is always to agree on what the correct logic is, documented in plain language, before writing a single line of SQL.

Building the warehouse first, asking the questions second. It is tempting to ingest everything into BigQuery and figure out the models later. In practice, this creates a raw data swamp that costs money to store and query but delivers nothing to the close process. Start with the three or four questions the finance team needs answered on day one of the close — settlement vs. ledger, fees paid vs. fees invoiced, cash in vs. expected — and model backwards from those.

Neglecting data contracts with source systems. When a PSP changes its export format, or a banking API changes its field names, a fragile ingestion pipeline silently starts loading bad data. Most teams still face fragmented data, manual processes, and dependencies across the business that drag out their close timeline. Building explicit schema validation at the ingestion layer — tests that fail loudly when expected fields are missing or malformed — is the difference between a pipeline that alerts on failure and one that fails silently.

Underinvesting in the business logic layer. The reconciliation rules in a growth-stage fintech or payments company are not simple. Multi-currency settlement, timing differences between transaction date and value date, partial refunds, disputed transactions — each of these is a test case that needs to be written and pass before the model goes to production. The dbt testing framework is your friend here. If you are seeing unexplained slowness or brittleness in your existing models, Why Your dbt Models Are Running Slow — And How to Fix It covers the optimisation patterns in detail.

Building dashboards nobody trusts. A close dashboard is only useful if finance is prepared to rely on it instead of the spreadsheet. That transition requires a period of parallel running — showing both the old and new numbers side by side, investigating every discrepancy, and building confidence incrementally. Skipping this step and expecting instant adoption is a reliable way to see a well-engineered solution ignored.

Frequently Asked Questions

Q: What is financial close analytics?

A: Financial close analytics is the use of automated data pipelines, SQL transformation models, and BI dashboards to replace manual spreadsheet-based processes in the monthly financial close cycle. It enables finance teams to produce accurate, auditable financial statements faster and with less manual effort — typically reducing close time from 5–10 days to 1–3 days.

Q: How long should a month-end close take?

A: Best-in-class finance teams close in three days or fewer. According to 2025 benchmark data, only 18% of teams currently achieve this — half still take longer than a week. A well-engineered financial close analytics stack is the primary lever for moving from a slow close to a fast one at growth-stage companies.

Q: Can dbt be used for financial close automation?

A: Yes — dbt is well suited to modelling reconciliation logic, financial transformations, and metric definitions that currently live in spreadsheets. It adds version control, automated testing, and documentation to calculations that are otherwise brittle and undocumented. Many growth-stage fintechs and payments companies have migrated their close logic into dbt models with significant reductions in close time and error rates.

Q: What data warehouse is best for financial close analytics?

A: BigQuery is the most common choice for growth-stage companies due to its serverless architecture, low operational overhead, and strong integration with modern data tools like dbt and Holistics BI. Snowflake and Redshift are also viable depending on existing infrastructure. The warehouse choice matters less than the quality of the modelling and governance layers built on top of it.

Q: How do I know if my financial close process needs a data engineering fix?

A: If your close relies on manual CSV exports from multiple systems, calculations in spreadsheets that only one person fully understands, or produces different numbers in different reports, the root cause is almost always a data infrastructure gap rather than a process or headcount problem. Automating the underlying pipelines and models is the durable fix.

At Fintel Analytics, we have helped fintech, payments, and e-commerce businesses at every stage from pre-seed to Series B replace broken, manual close processes with automated SQL pipelines, governed dbt models, and live finance dashboards — going from a week-long close to a two-day one, and from numbers nobody trusts to a single source of truth that the CFO, board, and auditors all work from. If your finance team is still spending the first week of every month chasing the same numbers across the same spreadsheets, that is a solvable problem — and the time and cost savings are quantifiable from day one.