Digital Wallet Analytics: Fix Broken Balance & Transaction Data in 2026

Digital wallet analytics breaks when the underlying transaction data isn't modelled correctly — producing balance discrepancies, conflicting metrics, and reports your finance team refuses to trust. The fix is not a better dashboard; it's a properly engineered data layer that models wallet state, ledger movements, and FX flows as first-class analytical objects.

In 2024, the global total value of digital wallet transactions reached $10 trillion. The global digital wallet market is expected to grow at a 28.3% average annual compound rate to a total of $51.5 billion. Behind every one of those transactions sits a data engineering problem that most growth-stage fintechs have not yet solved. The wallets work. The balances settle. But the analytics layer — the part that answers "why did our float drop this week?", "which corridors are generating fee revenue?", "what is our average wallet lifetime value?" — is either missing entirely, or cobbled together from exports, spreadsheets, and half-built SQL queries that nobody fully trusts.

If that sounds familiar, this post is for you.

Why Digital Wallet Analytics Is Harder Than It Looks

The surface problem looks simple: you have a transaction log, you have wallet balances, you produce some reports. In practice, wallet data is structurally more complex than most other fintech transaction types, and it breaks analytics in specific, predictable ways.

First, wallet transactions are stateful. Unlike a payment that has a clear debit and credit, a wallet balance is the accumulation of many events — top-ups, transfers, FX conversions, fee deductions, reversals, chargebacks, and sometimes manual adjustments. If your analytics layer is computing balance from a sum of transactions, a single missed event or incorrectly typed reversal will produce a wrong number — and you may not notice for days.

Second, wallet products typically run across pooled accounts. Accurately tracking all deposits, transfers, and FX movements across user wallets is non-trivial — especially when you need to maintain internal ledgering with pooled IBANs or custody structures. From an analytics standpoint, this means you cannot simply group by account number. You need a data model that understands the relationship between internal wallet IDs, virtual account structures, and underlying bank account balances.

Third, multi-currency complicates every metric. A wallet product operating across ten currencies does not have one revenue number — it has ten, plus the FX gain/loss layer sitting beneath them. Reporting consolidated wallet revenue without a properly modelled FX conversion layer produces a figure that is directionally correct but analytically useless for operational decisions.

A pattern we see repeatedly: a fintech's finance team is running a consolidated wallet revenue report from a BI tool, and separately a finance analyst is maintaining a parallel spreadsheet because "the dashboard doesn't account for FX correctly." Two numbers exist. Nobody is sure which one is right. Decisions get made on gut feel. This is fixable — but only if you address it at the data model layer, not the dashboard layer.

📺 Watch: A FinTech Analysis of eWallet and Digital Transfer Systems by Heng Shi Ying

What a Broken Wallet Analytics Stack Actually Looks Like

The failure modes are consistent enough that we can describe them precisely.

Balance drift. Computed wallet balances in your analytics warehouse diverge from source-of-truth balances in your operational ledger over time. This happens when your pipeline misses late-arriving events (common with payment network settlement data), processes reversals incorrectly, or applies FX rates at the wrong point in the event stream. The drift starts small — a few cents across a few wallets — and compounds until someone notices a rounding discrepancy in a monthly report. By that point, you have no clean audit trail back to the source.

Metric fragmentation. Finance calculates wallet revenue from the general ledger export. Product calculates it from the transaction log. Operations calculates it from a fee schedule spreadsheet. All three produce different numbers. Most fintechs start tracking money in Excel, graduate to repurposing their general ledger, then eventually face a reckoning when reconciliation breaks, auditors ask questions, or a regulatory filing deadline looms. The reckoning is avoidable — but only if you build a single, version-controlled metric layer before the numbers diverge.

Missing event types. Wallet products generate a wide variety of event types: top-ups, withdrawals, internal transfers, P2P sends, fee charges, FX conversions, cashback credits, referral bonuses, chargebacks, and administrative adjustments. Most analytics pipelines are built to handle the happy path — top-up and withdrawal — and the edge cases get handled ad hoc, or not at all. When your analytics model silently drops adjustment events, your reported wallet float is wrong every time an ops team member posts a correction.

No wallet lifetime view. The most analytically valuable question — what does a wallet's full lifecycle look like, from activation through to dormancy or closure? — is almost never answerable from a poorly structured wallet data model. You can count active wallets. You cannot tell your investors a wallet cohort's three-month revenue per user, or which acquisition channel produces wallets with the best long-term float retention.

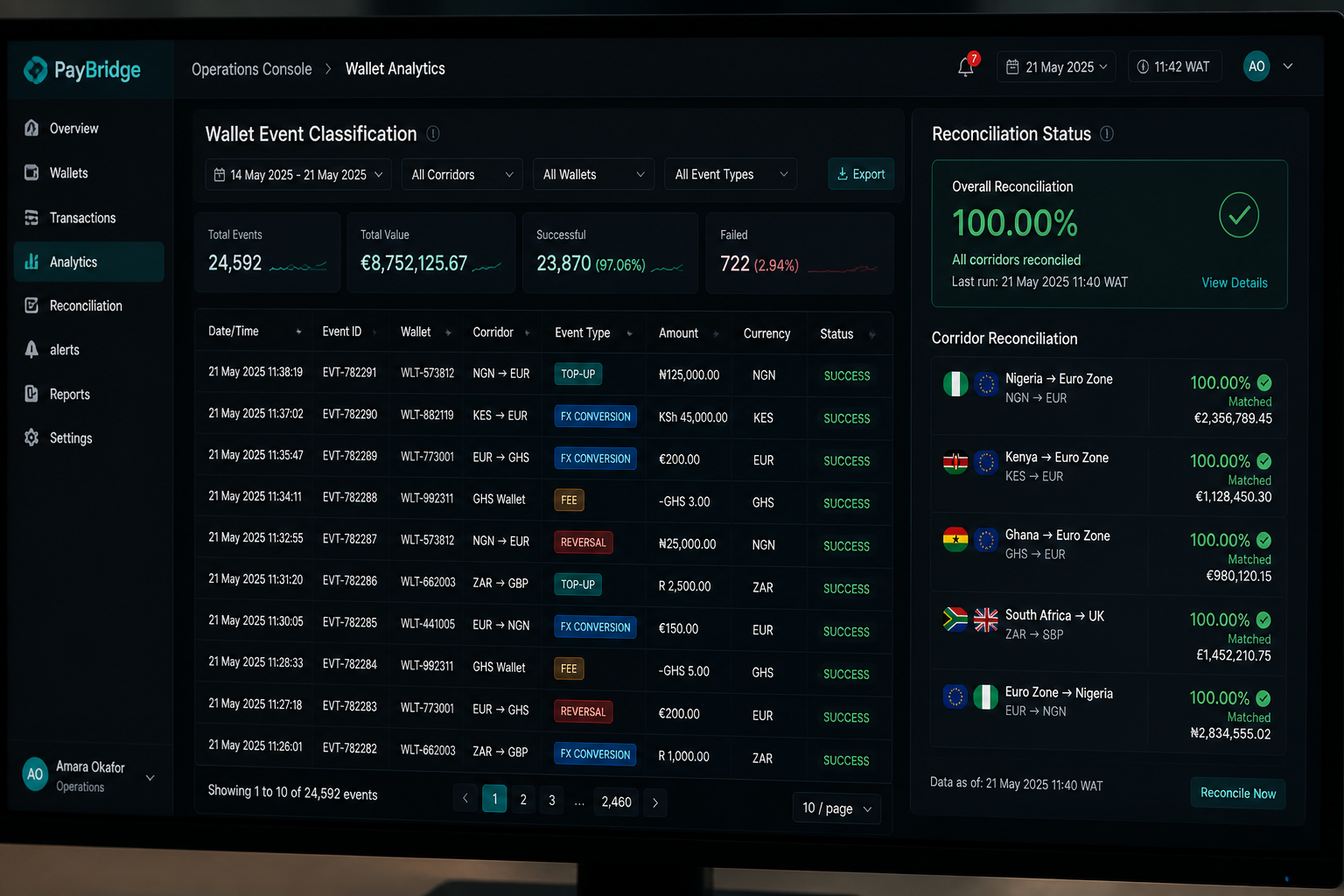

We rebuilt the analytics layer for a Series A digital wallet provider operating across four African markets. Their original pipeline was summing transaction amounts by wallet ID to derive balances — no event-type classification, no FX rate joining, no handling of reversals. The balance discrepancy between their analytics warehouse and their operational system was averaging 2–4% across the book. For a business managing multi-million dollar float, that gap was material. After modelling wallet state correctly in dbt, with event classification and FX normalisation baked in, the discrepancy dropped to zero and stayed there.

How to Model Wallet Transaction Data Correctly

The architecture that works — and that we have delivered across multiple wallet and payments clients — follows a consistent pattern.

Layer 1: Raw event ingestion with full fidelity. Every wallet event must be ingested in its original form, with its original timestamp, event type, and metadata. Do not aggregate, filter, or transform at this layer. The most common mistake is discarding "low-value" event types at ingestion — small FX conversions, micro-fee deductions, adjustment credits — because they seem analytically irrelevant. They are not. They are the difference between a balance that reconciles and one that doesn't.

Layer 2: Event classification in dbt. Build a staging model that classifies every wallet event into a controlled taxonomy: TOP_UP, WITHDRAWAL, INTERNAL_TRANSFER, FX_CONVERSION, FEE_CHARGE, REVERSAL, ADJUSTMENT, and so on. This classification is the backbone of every downstream metric. If it's wrong, everything built on top of it is wrong. Version control it, test it, and never let it live in a dashboard calculation.

Layer 3: Wallet state model. Build a model that computes wallet balance as a running sum of signed event amounts, grouped by wallet ID and currency. Use window functions, not aggregates. You want to be able to reproduce the exact balance at any point in time — not just the current balance. This is the model that your finance team needs for reconciliation and that your compliance team needs for audits.

Layer 4: FX normalisation. Join each event to the appropriate exchange rate at the time of the event — not the current rate, not a daily close rate, but the transaction-time rate. Store both the original currency amount and the normalised amount. Never convert at query time inside a dashboard; it introduces inconsistency every time exchange rates change. Track balances and transactions in any currency, with FX conversion applied consistently — and either handle gains and losses or isolate per-currency ledgers.

Layer 5: Metric layer. Only once layers 1–4 are stable and reconciled do you build your business metrics: active wallet count, wallet revenue per user, float by currency, average transaction value by corridor, fee yield by product type. These live in a SQL semantic layer — we use dbt metrics and Holistics BI for most clients — so that every team is reading the same number from the same calculation, not each running their own SQL.

If you want to explore how this architecture maps to your specific wallet product, explore how Fintel Analytics approaches data engineering for fintech companies — we design and deliver exactly this kind of solution for growth-stage businesses globally.

The Reconciliation Problem: Where Most Pipelines Break

Reconciliation is where the gap between a theoretically correct data model and a production-grade analytics pipeline becomes visible. Most wallet analytics pipelines reconcile in development. They break in production — and they break in specific, predictable ways.

Late-arriving data. Payment network settlement files arrive hours or days after the transaction. If your pipeline runs once per day and processes events in arrival order, your real-time balance is understated every time a batch arrives late. The fix is a pipeline architecture that handles late-arriving events gracefully: idempotent inserts, event-time partitioning, and a reconciliation flag that marks balances as "provisional" until the settlement file confirms them.

Duplicate events. Payment networks and internal systems both generate duplicate event records — retry logic, double-posting bugs, webhook retries. A pipeline that does not deduplicate at the ingestion layer will overcount every metric it produces. We have seen this produce a 3–5% overstatement of wallet revenue in pipelines that had been running for over a year without anyone noticing.

Reversal handling. A reversal is not the same as a negative transaction. It is a new event that references a prior event and cancels its effect. A data model that treats a reversal as a negative transaction will produce correct totals but will misclassify the event type — meaning your fee revenue, your top-up volume, and your transaction counts will all be wrong even if your net balance figure is right.

Real-time settlement creates real-time reconciliation problems. As payment rails move toward instant settlement, the window for catching discrepancies before they compound shrinks. A reconciliation process that ran acceptably as a daily batch job becomes untenable when transactions settle in seconds.

We rebuilt a reconciliation process for a global payments provider that was taking 30–50 minutes to run against their growing transaction history. It was rebuilt as an automated SQL pipeline in BigQuery with proper partitioning and incremental processing — it now completes in under 3 seconds, and flags exceptions in real time rather than the next morning.

For teams who are also managing multi-currency wallet balances, the interaction between reconciliation and FX creates additional complexity — see our post on Multi-Currency Analytics: Fix Broken Financials in 2026 for a deeper treatment of that specific problem.

What Good Wallet Analytics Actually Enables

Once the data engineering foundation is correct, wallet analytics stops being a reporting task and starts being a strategic capability. Here is what becomes possible.

Float optimisation. With accurate, real-time wallet balance data segmented by currency and geography, a treasury team can actively manage float — pre-funding corridors that are consistently undersupplied, identifying dormant balances that can be redeployed, and setting alert thresholds for funding risk. This is not possible when your balance data has a known reconciliation error and a 24-hour lag.

Wallet cohort analysis. 4.5 billion consumers used digital wallets in 2025, with digital wallet usership growing to 5.2 billion in 2026. In a market this competitive, the companies that win are not the ones that acquire the most wallets — they are the ones that activate the most and retain the best. That distinction requires a cohort analytics layer: wallet activation cohorts, revenue cohorts, and dormancy prediction models. None of this is possible without a wallet state model that tracks every wallet's full event history. For a deeper look at building retention cohorts correctly, see our post on Cohort Analysis for Startups: Why Your Retention Numbers Are Lying to You.

Fee and yield analytics. Most wallet products generate revenue through a combination of transaction fees, FX margin, and subscription charges. Understanding which of these yields the most per active wallet — and which product features drive the highest-yielding wallet behaviour — requires a data model that correctly classifies and attributes every revenue event. We built this for an e-money institution operating across six European markets, and it allowed them to identify that a specific top-up channel was generating wallets with 40% higher 90-day revenue than their default channel — a finding that directly informed their next acquisition spend allocation.

Regulatory and audit readiness. In many cases, businesses do not realise the full consequences of ledger inadequacies until it is too late — such as in the case of Synapse, where gaps in ledgering reportedly contributed to millions of dollars in unreconciled customer funds and a highly publicised operational collapse in 2024. A well-engineered wallet analytics layer, with full event history, event-time timestamps, and reconciliation flags, is not just an operational tool — it is an audit artefact. When a regulator or investor asks for a point-in-time view of wallet balances on a specific date, you need to be able to produce it from your data warehouse, not reconstruct it from six months of transaction exports.

Provider performance benchmarking. Multi-sided platforms splitting payments across sellers, service providers, tax jurisdictions, and escrow accounts generate reconciliation complexity that grows exponentially with scale. With a correctly structured wallet analytics layer, you can benchmark performance by underlying payment provider, by corridor, and by product type — identifying which settlement partners are slow, which corridors have anomalous failure rates, and where fee leakage is occurring.

Frequently Asked Questions

Q: What is digital wallet analytics and why does it matter for fintech companies?

A: Digital wallet analytics is the practice of modelling, measuring, and analysing wallet transaction data — including balance movements, FX flows, fee revenue, and user activity — to support operational decisions, reconciliation, and product strategy. It matters because wallet products generate complex, stateful data that breaks standard analytics approaches. Without a properly engineered analytics layer, fintechs operate with balance discrepancies, conflicting metrics, and no reliable basis for decisions about float, fee yield, or user retention.

Q: Why do wallet balance figures differ between my analytics dashboard and my operational system?

A: Balance discrepancies between analytics and operational systems are almost always caused by one or more of: late-arriving settlement events, incorrect reversal handling, missing event types at ingestion, or FX conversion applied at the wrong point in the pipeline. The fix requires rearchitecting the data pipeline to process events in event-time order, handle all event types including edge cases, and reconcile against the operational ledger on a continuous basis — not just at month end.

Q: What data infrastructure do I need to run wallet analytics at Series A scale?

A: At Series A scale — typically tens of millions of wallet events per month — the right stack is a cloud data warehouse (BigQuery or Snowflake), a transformation layer in dbt with proper testing and incremental models, and a BI tool connected to a SQL semantic layer. The critical investment is in the dbt modelling layer: wallet state models, event classification, and FX normalisation. The dashboard is secondary. If the models are right, reporting is straightforward. If they are wrong, no dashboard can fix it.

Q: How do I reconcile wallet data across multiple payment providers?

A: Multi-provider wallet reconciliation requires a unified event schema that normalises events from every provider into a common taxonomy before any analysis is performed. Each provider will use different field names, different event type codes, and different timestamp conventions. Build provider-specific staging models in dbt that translate each source into your canonical schema, then run reconciliation logic against the normalised layer — not against raw provider data. This allows you to compare like-for-like across providers and detect discrepancies at the event level.

Q: What metrics should a fintech track for digital wallet performance?

A: The core wallet performance metrics are: active wallet count (by cohort and acquisition channel), float by currency and geography, average revenue per active wallet (by fee type), wallet activation rate, wallet dormancy rate and timing, FX yield per conversion event, and provider settlement lag by corridor. These should be defined once in a SQL semantic layer and consumed consistently across finance, product, and operations teams — not calculated independently in each team's spreadsheet or ad-hoc query.

Building reliable digital wallet analytics is not a dashboard problem — it is a data engineering problem, and it compounds silently until a reconciliation failure, an audit request, or a fundraise surfaces the gap at the worst possible moment. At Fintel Analytics, we have helped digital wallet providers, e-money institutions, and multi-currency payment platforms build the exact data infrastructure described in this post — from event ingestion and dbt modelling through to live operational dashboards and regulatory-grade audit trails. If your wallet data is producing numbers your finance team doesn't trust, that is a solvable problem, and solving it typically unlocks analytical capabilities your team has been unable to act on for months.