Credit Risk Analytics for Fintech Lenders: Build It Right in 2026

Credit risk analytics for fintech is not primarily a machine learning problem — it is a data engineering and infrastructure problem. Most lenders that struggle with model accuracy, slow decisioning, or regulatory scrutiny can trace the root cause to the same place: fragile pipelines, unvalidated inputs, and credit logic buried in spreadsheets no one fully controls. Fix the foundation, and the models follow.

In the fintech era, the evolution of credit scoring systems is being rapidly accelerated by advances in machine learning and data analytics. But acceleration without infrastructure is how you end up approving loans on bad data and explaining yourself to a regulator. Challenges remain — 65% of lenders report difficulties in obtaining AI-ready data, even though 89% recognise AI as critical to the lending process. (2026)

In our work with growth-stage lending businesses, we see a consistent pattern: the ML model is fine; the data feeding it is the problem. Features are computed differently across environments, validation is inconsistent, and the only person who truly understands the scoring logic left the business six months ago. This post is a practitioner's guide to building credit risk analytics infrastructure that actually holds up — in production, under audit, and at scale.

Why Most Fintech Credit Models Break Before They Scale

The textbook version of credit risk modelling is clean: ingest data, engineer features, train a model, deploy, monitor. The reality in a growth-stage fintech looks very different.

A pattern we see repeatedly: the original credit model was built by a data scientist who joined at seed stage, trained on a sample of early applications, and deployed into a notebook-based pipeline that runs manually every morning. It worked at 500 applications a month. At 5,000, it starts to crack — not because the model is wrong, but because the pipeline cannot reliably produce consistent, validated inputs at volume.

The accuracy and reliability of results will depend on the data used. Poor-quality data can lead to inaccurate credit assessments. That sounds obvious, but the failure mode is subtle: the model does not crash — it just quietly produces scores based on stale, mismatched, or malformed features, and no one knows until the default rate drifts.

Traditional scoring methods leave too many gaps — slow decisions, limited data coverage, and exclusion of new-to-credit customers. AI credit scoring platforms, by contrast, draw on broader datasets, improving prediction accuracy and enabling faster, fairer decisions. But that broader dataset only delivers if your data pipeline can actually ingest, normalise, and validate it consistently.

The most dangerous setup we encounter is a fintech where:

- Bureau data lands in raw JSON and gets parsed inconsistently between dev and production environments

- Alternative data signals (transaction history, open banking feeds) are joined with different lag windows across environments, producing training-serving skew

- The credit score itself is recalculated in two places — once in the ML model and once in a Google Sheet used by the credit committee — and they disagree

- Nobody has documented which version of a feature definition is canonical

That last point is not a modelling failure. It is a governance failure, and it is far more common than anyone publishes about.

📺 Watch: Credit Analysis Fundamentals: How Banks & Lenders Assess Creditworthiness Part 1 | CFI Course

What "AI-Ready" Credit Data Actually Requires

Building a credit risk analytics capability that works starts with treating data as the product, not an input. Here is what that means in practice.

1. A single validated source of truth for every credit feature

Every feature used in decisioning — bureau score, days-since-last-derogatory, monthly transaction volume, open banking balance trajectory — should be defined once, in a dbt model in your data warehouse, and consumed from there. Not recomputed in application code, not duplicated in a notebook, not approximated in a spreadsheet. One definition. One place.

We have consistently found that migrating feature calculations from ad-hoc scripts and spreadsheets into dbt models eliminates a whole class of scoring inconsistencies and cuts the time credit teams spend investigating "why does this applicant have two different scores?" to near zero. The pattern mirrors a broader outcome we have seen across clients: migrating calculations from spreadsheets into dbt models eliminated recurring manual errors and cut weekly maintenance time by 30 minutes — and in credit, the stakes of those errors are far higher.

2. Validated inputs with schema contracts

The challenge with alternative data is not sourcing it — it is integrating it into a decisioning workflow that can act on it in real time. Bureau feeds arrive in different schemas across providers. Open banking connections drop and reconnect with schema changes. Telco data arrives in batches with inconsistent null handling.

Every upstream data source feeding your credit model needs a data contract: expected schema, acceptable value ranges, freshness SLA, and an automated test that fails loudly if the contract is violated. In dbt, this is a combination of schema tests, custom generic tests, and source freshness checks. The moment a bureau feed starts returning unexpected nulls on a key field, your pipeline should halt and alert — not silently pass through zeroes that your model treats as meaningful signal.

For a deeper look at how to implement this kind of test coverage, our post on dbt Testing Strategy for Startups covers the pattern in detail.

3. Feature pipelines that are identical in training and serving

Training-serving skew is the silent killer of credit models in production. You train on historical features computed one way; at inference time, the live pipeline computes them slightly differently — different join logic, different time window, different handling of missing values. The model appears to work in backtesting and immediately underperforms in production. Models degrade over time as borrower behaviour and market conditions change — a problem known as model drift. But skew-induced degradation is not drift; it is a pipeline defect masquerading as one.

The fix is a shared feature store or, for smaller teams, a single set of dbt models that serves both historical training data and live inference inputs. Training runs against a snapshot of the same SQL logic that scoring runs against in production. If the logic changes, it changes in one place, and both training and serving inherit the update.

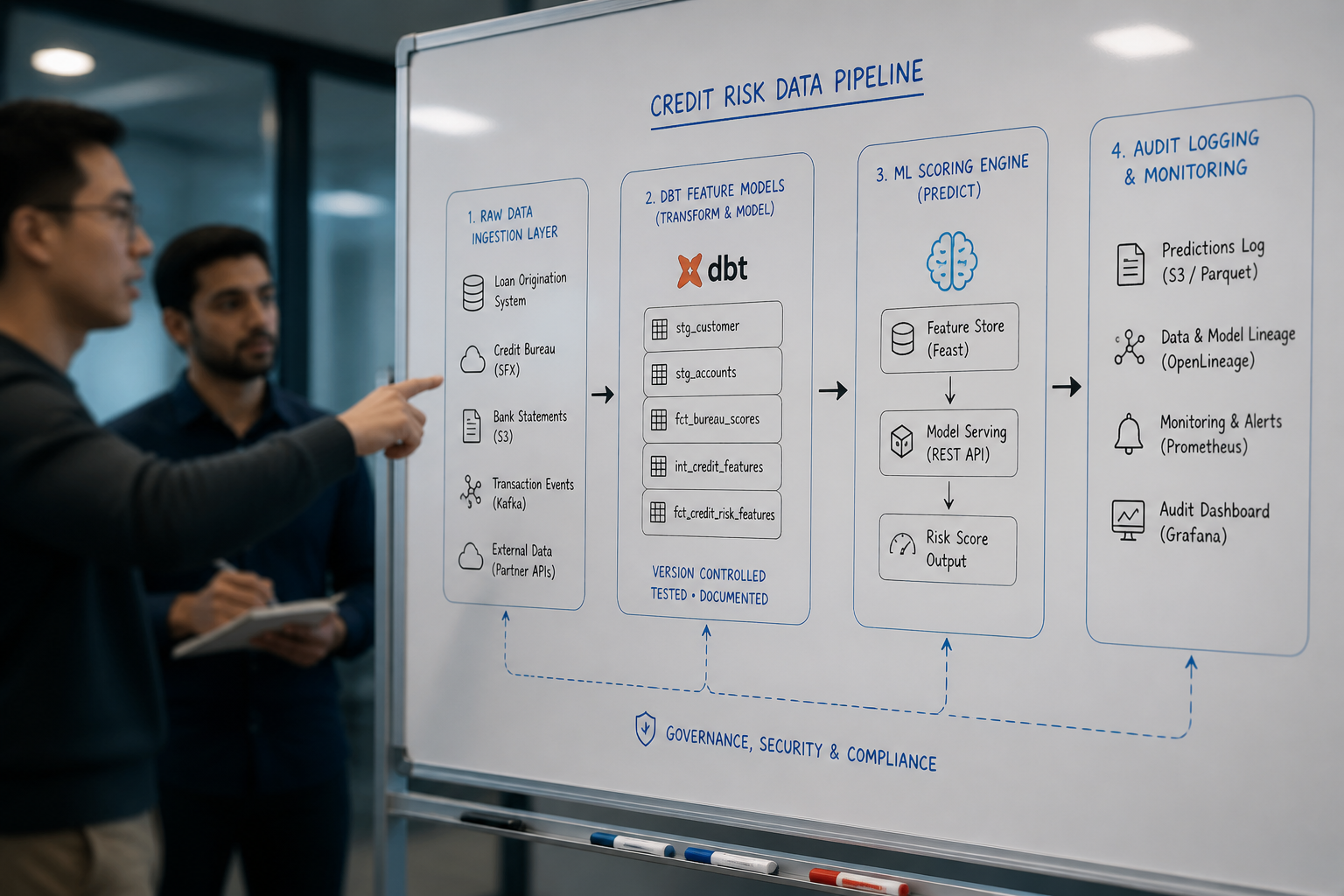

How to Structure a Credit Risk Analytics Stack

The following architecture is what we recommend and build for growth-stage fintech lenders operating on modern cloud infrastructure (BigQuery or AWS Redshift, dbt, with a BI layer for credit operations dashboards).

Ingestion layer Raw data from bureau APIs, open banking providers, internal transaction databases, and any alternative data sources lands in a raw schema in BigQuery. Nothing is transformed here. Data lands as-received, timestamped, and immutable. This is your audit trail.

Staging and validation layer (dbt) Staging models cast types, rename columns to canonical names, and apply source freshness and schema tests. If a bureau response is malformed, it fails here. This layer exists to protect everything downstream from bad inputs.

Feature layer (dbt) Credit features are computed here: rolling transaction aggregates, bureau score deltas, payment-to-income ratios, delinquency flags, open banking balance trends. Each feature model is documented with a business definition, the data source it draws from, and the test coverage it carries. This is your single source of truth for credit feature definitions.

Model serving layer For real-time decisioning, the feature layer outputs are either queried directly at inference time (for low-latency requirements over pre-aggregated features) or pushed to a feature store for sub-100ms lookup. The ML model itself — typically an XGBoost or gradient-boosted ensemble for structured credit data — sits in a separate serving environment and reads from this layer.

Monitoring and BI layer A credit operations dashboard (we typically build these in Holistics BI or Looker) gives the credit team live visibility into: approval rates by segment, score distribution shifts, feature drift indicators, and model performance metrics (Gini, KS statistic, PSI). When something moves, the team sees it — they do not wait for the monthly model review to find out the score distribution has shifted.

AI-powered credit scoring platforms solve these challenges by combining automated financial data extraction, predictive scoring models, real-time risk monitoring, and ERP-integrated decision workflows. Modern AI credit scoring software continuously analyses payment behaviour, financial statements, external bureau data, and real-time risk alerts to automate low-risk approvals, prioritise high-risk reviews, and standardise credit decisioning across customer portfolios.

If you are building or rebuilding a credit analytics stack and want to understand what this looks like for your specific data environment, explore how Fintel Analytics approaches this — we work with fintech lenders globally to design and deliver exactly this kind of infrastructure.

The Explainability Requirement You Cannot Ignore in 2026

If your credit scoring model cannot explain why it denied a specific applicant, it is not just a model quality problem — it is a compliance problem.

The central mandate from the CFPB is explainability. The bureau has explicitly stated that creditors cannot use "black-box" underwriting technology if it prevents them from providing specific and accurate reasons for adverse actions as required by law.

The regulatory environment has become even more stringent in 2026. The Financial Services AI Risk Management Framework, introduced in February 2026, outlines 230 control objectives spanning governance, data handling, and model development. Startups must also comply with regulations like the EU AI Act (which classifies lending as high-risk), GDPR, and the CFPB's Personal Financial Data Rights Rule.

In practice, explainability for credit models means two things: model-level interpretability (SHAP values that tell you which features drove a given score) and decision-level documentation (audit logs that record the exact feature values, score, and decision reason code for every application, immutably). Shift toward explainable AI (XAI) or "white box" models. Use explainability tools such as SHAP and LIME to interpret model outputs. Establish model audit and documentation procedures to ensure traceability.

The engineering implication is that your serving pipeline must log not just the decision, but the feature vector that produced it — with version tracking on both the feature definitions and the model version. If a regulator asks why applicant 47,832 was declined in March, you need to be able to reproduce the answer from immutable logs. Most growth-stage lenders cannot do this today.

AI scoring models should sit inside a formal model risk management framework with clear ownership, independent validation, change control, performance monitoring, and documented limitations. For US-regulated lenders, this governance model is anchored in SR 11-7 and OCC model risk guidance; the OCC updated that guidance in April 2026, but the core expectation remains the same: models must be controlled, validated, and auditable throughout their lifecycle.

This is also where having a well-governed feature layer pays dividends beyond modelling accuracy. When every feature is defined in a documented dbt model with version control, your model governance documentation writes itself: you can point a regulator at the exact SQL that computed the feature used in a declined decision.

Alternative Data: The Opportunity and the Infrastructure Trap

Machine learning algorithms evaluate creditworthiness using alternative data sources beyond traditional credit scores, including transaction history, utility payments, and digital footprints. For fintech lenders targeting underserved borrowers, this is the competitive opportunity — extending credit to applicants with thin bureau files by using richer behavioural signals.

The global alternative business credit scoring (non-bureau) market was valued at USD 2.67 billion in 2025 and is projected to grow from USD 2.96 billion in 2026 to USD 5.92 billion by 2034, exhibiting a CAGR of 9.0%.

These approaches leverage real-time data such as cash flow patterns, invoice payment histories, bank transactions, digital footprints, and supply chain interactions. Key components include AI-driven algorithms, machine learning models, open banking integrations, and trade credit analytics.

But here is the infrastructure trap that catches most lenders: alternative data sources are messy by default. Open banking feeds have inconsistent transaction categorisation across providers. Telco data arrives in proprietary schemas. Cash flow data requires normalisation across multi-currency accounts before it is usable. Raw, it is not credit signal — it is noise.

The normalisation work required to turn alternative data into reliable model features is typically 60–70% of the total effort in building an alternative data credit programme. Teams underestimate it because it looks like "just data preparation" — until they realise that "cash flow volatility over the past 90 days" means something different for a freelancer paid in irregular lumps than for a salaried employee, and that difference needs to be encoded in the feature logic, not handled by the model.

For fintechs operating cross-border, there is an additional layer: currency normalisation and jurisdiction-specific feature logic. A feature that is predictive in one market may be meaningless in another. We covered the complexity of multi-currency data handling in our post on Multi-Currency Analytics: Fix Broken Financials in 2026 — many of the same data pipeline challenges apply directly to cross-border lending.

Frequently Asked Questions

Q: What data infrastructure does a fintech lender need for credit risk analytics?

A: At minimum: a cloud data warehouse (BigQuery or Redshift) as your single source of truth, dbt for validated feature engineering, a BI layer for credit operations monitoring, and immutable audit logging for every decision and the feature vector that produced it. The ML model itself is the smaller part of the investment.

Q: How do you prevent training-serving skew in a credit scoring pipeline?

A: By computing features in a single place — typically a shared set of dbt models — that serves both historical training data and live inference inputs. When both training and serving run from the same SQL logic, skew becomes structurally impossible rather than something you diagnose after the fact.

Q: What does the EU AI Act mean for fintech credit scoring in 2026?

A: The EU AI Act classifies automated credit decisioning as high-risk AI, which means full explainability, bias testing, audit trails, and human-review pathways are now legal requirements, not best practices. The high-risk AI rules apply from August 2026. Every lender using automated scoring in the EU should have governance documentation and explainability tooling in place now.

Q: How should growth-stage fintechs handle model monitoring for credit risk?

A: Track three things continuously: Population Stability Index (PSI) on incoming feature distributions, model performance metrics (Gini, KS) on scored cohorts, and approval rate trends by segment. When PSI on a key feature exceeds 0.2, treat it as a signal that either the input data has changed or the population has shifted — and trigger a model review before default rates confirm it.

Q: What is the biggest mistake fintech lenders make with credit analytics?

A: Investing in model sophistication before fixing the data pipeline. A well-engineered logistic regression on clean, validated, consistently defined features will outperform a gradient-boosted ensemble trained on inconsistent data from fragmented sources. The model is never the bottleneck. The data is.

Building credit risk analytics that hold up under volume, regulatory scrutiny, and organisational change requires getting the data infrastructure right before — not after — you optimise the model. At Fintel Analytics, we have worked with growth-stage fintech lenders to build exactly this kind of foundation: validated feature pipelines in dbt, credit operations dashboards that give risk teams real-time visibility, and audit-ready decisioning infrastructure that survives both scale and due diligence. If your credit scoring stack is held together by notebooks and spreadsheets and you are approaching the point where that breaks, the time to fix it is before the next funding round — not after.