KYC/AML compliance analytics is the practice of ingesting, modelling, and surfacing data from identity verification, transaction monitoring, and case management systems so that compliance teams can operate efficiently, regulators can be satisfied, and leadership can quantify risk in real time. Done well, it replaces manual case reviews and spreadsheet audit trails with automated pipelines, a governed data model, and dashboards that track the metrics that actually matter — onboarding conversion, false positive rates, case resolution time, and SAR filing latency. Done poorly — or not done at all — it leaves compliance running on fragmented system exports and gut feel, which is increasingly a regulatory liability as well as an operational one.

The compliance data problem at most early-stage fintechs is not a shortage of vendors. It is a shortage of analytics infrastructure behind those vendors. Most Series A payments companies we work with have integrated a KYC provider, a transaction monitoring tool, and a case management system within the first 12 months of operation. What they almost never have is a unified data layer that connects those three systems, normalises their outputs, and makes the combined data queryable. The result: compliance leadership cannot answer basic questions — how many accounts are stuck in review right now, how long has each one been waiting, what share of alerts last month were false positives, and is that share improving or getting worse?

That gap is no longer acceptable. Regulatory pressure in 2026 is measurably higher than it was two years ago, and the cost of failing to instrument your compliance function correctly is now both financial and existential.

Why Compliance Analytics Has Become a Business-Critical Data Problem

The numbers set the context clearly. A 2025 survey by Fenergo of 600 senior decision-makers across banks, asset managers, and fund administrators found that 70% of firms had lost prospective clients in the past year due to inefficient onboarding — up from 67% in 2024 and 48% in 2023. Fenergo separately estimated that abandoned KYC processes strip $3.3 billion annually from the banking sector. Meanwhile, the enforcement environment has sharpened dramatically. Global AML fines in the first half of 2025 alone reached $1.23 billion — a 417% increase on the same period in 2024.

For a fintech at Series A or Series B, neither of these dynamics is abstract. Every application that drops out of an onboarding funnel because KYC took too long is a unit-economics problem and an acquisition cost written off. Every manual process in your compliance function that could have been automated is an operating cost compounding as you scale. And every gap in your audit trail is a regulatory examination risk that, in 2026, carries real financial consequences.

The operational cost picture is similarly stark. Average annual spend on AML and KYC operations now stands at $72.9 million per firm across large financial institutions — with UK-based institutions reporting the highest costs at $78.4 million. Even at a fraction of that scale, the pattern holds: compliance functions that lack proper data infrastructure spend disproportionately on manual review, remediation, and rework. The data problem does not shrink as you grow; it compounds.

The adoption of AI in compliance is accelerating — use of advanced AI tools in KYC/AML operations jumped from 42% in 2024 to 82% in 2025. But that adoption is uneven and, critically, often sits on top of fragmented data foundations. AI on bad data produces confident wrong answers, not better compliance.

📺 Watch: What Is A KYC Analyst | Why Are AML/KYC Analysts Required | What Do Companies Look For When Hiring

What a Compliance Analytics Data Stack Actually Looks Like

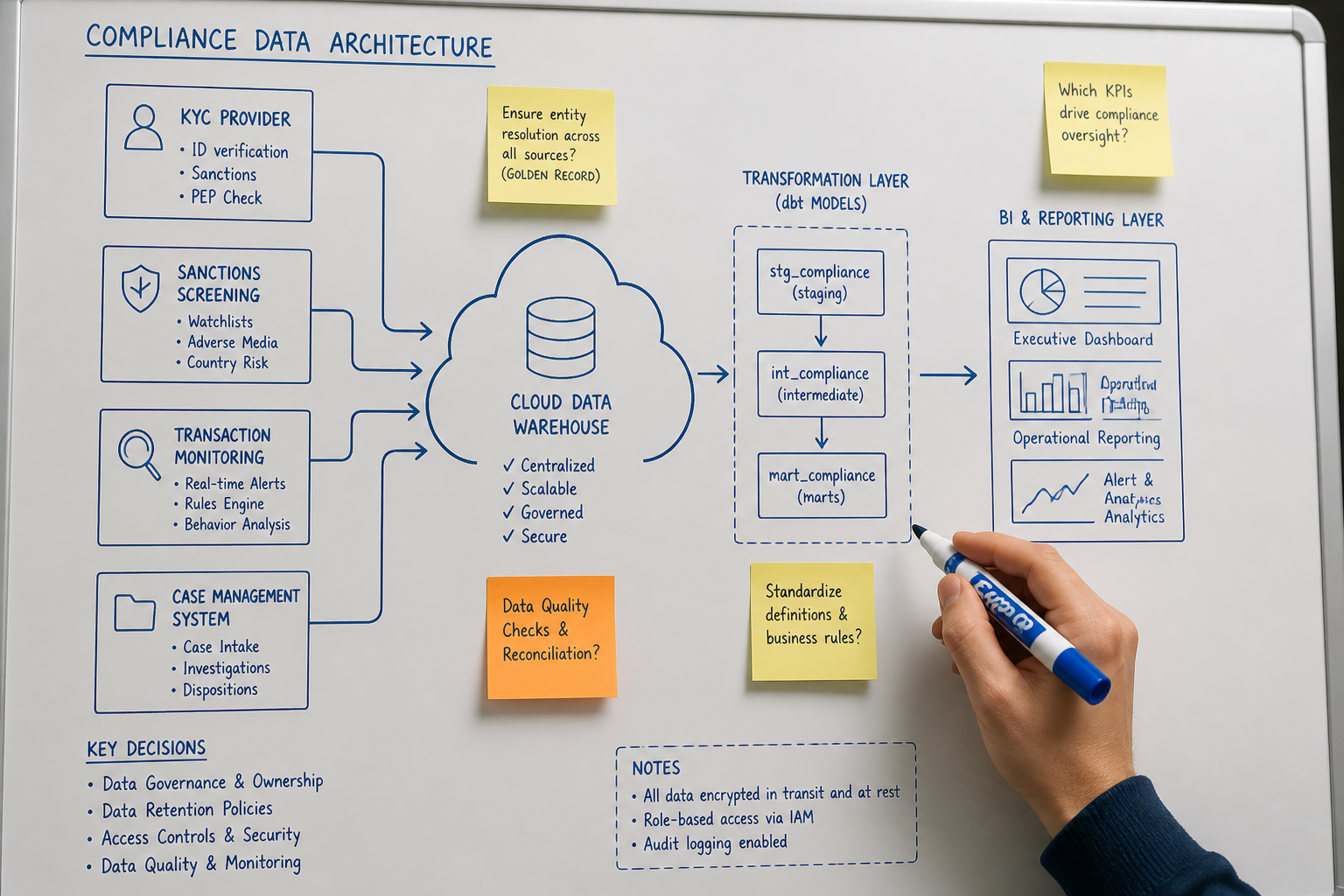

Most fintech compliance stacks involve at least four distinct systems: an identity verification provider (Jumio, Onfido, Sumsub, or similar), a sanctions and PEP screening tool, a transaction monitoring platform generating alerts, and a case management system where analysts work and disposition cases. Each of these typically has an API and/or a database export. None of them talk to each other natively at the data layer. Building the compliance analytics capability means building the connectors, the unified schema, and the models on top.

In practice, a well-architected compliance data stack for a growth-stage fintech looks like this:

Ingestion layer: Raw event feeds from each compliance system land in a cloud data warehouse — typically BigQuery or AWS (Redshift/S3) — via scheduled API pulls or change-data capture from operational databases. KYC decision events, alert trigger events, case open/close events, and SAR filing records each have their own ingestion pipeline. This is where data engineering matters most: the raw outputs from these systems are frequently inconsistent, use different identifiers for the same customer, and arrive with different latency characteristics.

Transformation layer (dbt): dbt models clean, join, and normalise the raw data into a compliance-specific semantic layer. Key models to build early: a unified customer profile model (linking KYC decision to account, to transaction history, to alert history, to case outcome), an alert lifecycle model tracking each alert from generation through disposition, and a case throughput model tracking analyst workloads and resolution times. These become the foundation for every compliance dashboard and regulatory report that follows.

Metrics and reporting layer: A BI tool — we typically deliver this in Holistics or Looker, depending on the client's needs and technical maturity — surfaces the metrics that compliance leadership and operations teams actually need day-to-day. This is not just a dashboard for the MLRO; it is also the operational data product for the analysts who are triaging cases and the finance team tracking the cost per review.

The critical design decision at this layer is governance. Compliance metrics must be defined once, in the semantic layer, not recalculated differently in every dashboard. False positive rate means exactly one thing across your organisation. Onboarding conversion rate through KYC means exactly one thing. When those definitions live in dbt models with proper testing and documentation, they are auditable — which matters enormously when a regulator asks how you calculated a metric.

If you want to see how Fintel Analytics designs and delivers analytics infrastructure for regulated fintech businesses, explore our services — we work with early-stage and growth-stage companies to build exactly this kind of foundation.

The Four Metrics Your Compliance Analytics Stack Must Track

Before diving into implementation detail, it is worth being opinionated about what you are actually trying to measure. A pattern we see repeatedly in early-stage fintechs is a compliance function that runs a KYC vendor and a transaction monitoring tool, produces some operational statistics for internal reporting, but has never defined — in a governed, consistent, queryable way — the metrics that would let leadership understand whether the function is performing or not. Here are the four that matter most:

1. KYC pass rate and drop-off by step. This is the funnel view of your onboarding process. What share of applicants pass document verification? What share clear sanctions screening? What share are referred to manual review, and of those, what share ultimately approve or decline? Without this model, you cannot distinguish a conversion problem caused by a broken UI from one caused by an overly aggressive risk threshold. One global payments company we worked with discovered through this analysis that 40% of their manual referrals were being approved — meaning the automated threshold was flagging a population that was almost entirely clean. Calibrating it saved both review cost and onboarding conversion.

2. Alert false positive rate by rule. In any rule-based or ML-driven transaction monitoring system, the false positive problem is real and expensive. Every alert that a human analyst has to review and close as a false positive is a cost — in analyst time, in throughput, and in the morale tax that comes with reviewing obvious non-events all day. Most fintech compliance teams know their overall alert volume; far fewer have a per-rule breakdown of true positive and false positive rates. Building this model in dbt — joining alert trigger data to case disposition data — typically takes one or two engineering sprints and immediately identifies which rules are generating disproportionate noise.

3. Case resolution time and analyst throughput. How long does the average case sit open? What is the distribution — are there a small number of very old cases aging out of control, or is the backlog evenly spread? Which case types take the longest, and why? These questions are answerable only if you have a properly modelled case lifecycle in your data warehouse. Without it, compliance managers are looking at a case management UI that shows a queue but gives no trend data, no SLA tracking, and no ability to forecast capacity needs.

4. SAR filing latency. Regulatory requirements around Suspicious Activity Report filing timelines are non-negotiable in most jurisdictions. Tracking the time from alert generation to SAR submission — and alerting when that gap approaches the regulatory deadline — is a compliance data product that should exist at every fintech handling material transaction volumes. SAR filing is one of the most common enforcement triggers; late filings represent a real and quantifiable regulatory risk.

The Perpetual KYC Data Architecture Problem

The industry is moving quickly toward perpetual KYC — continuous customer due diligence based on real-time data feeds and behavioural signals, rather than periodic static reviews. Some of the most advanced firms are now maintaining customer profiles that are continuously refreshed based on real-time data feeds, behavioural analytics, and external triggers like beneficial ownership changes or sanctions list updates.

This is the right direction. Periodic reviews done once every 12 or 24 months are a blunt instrument — they impose compliance cost on low-risk customers while potentially missing risk events in high-risk ones that occur between review cycles. A continuous model, properly instrumented, is both more accurate and more efficient.

But perpetual KYC creates a significant data engineering challenge that most discussions of the topic gloss over. A static periodic review is a batch process — pull a customer record, run the checks, record the outcome, repeat on a schedule. A continuous model requires event-driven architecture: a change in a customer's transaction pattern, a new sanctions list entry, a beneficial ownership update in a corporate registry — each of these must trigger a data event that flows into your compliance systems in near real time. That requires streaming ingestion, not just scheduled batch pulls.

For most pre-Series B fintechs, building full event-driven perpetual KYC architecture is premature. What is not premature is building the data model that makes the transition possible when you reach the scale where it matters. Specifically: modelling your customer risk score as a time-series entity (not a static field), storing the full history of every KYC check outcome against a customer, and building the data infrastructure that would let you trigger re-review events programmatically when upstream signals change. These design decisions are cheap to get right early and expensive to retrofit at scale.

A pattern we observe consistently in our work with early-stage companies is a compliance data model built around the operational system rather than the analytical use case — a direct replica of the KYC vendor's data structure, rather than a model designed for the questions compliance leadership actually needs to answer. The vendor schema is optimised for transaction processing. Your data warehouse schema should be optimised for analysis. They are different, and conflating them is the root cause of most compliance reporting pain.

What a Well-Instrumented Compliance Function Actually Looks Like

Let me make this concrete with a pattern from delivery experience. A Series A payments company operating across multiple jurisdictions was handling material onboarding volumes but running compliance reporting almost entirely from manual case management exports into spreadsheets. The compliance manager would pull a weekly CSV, pivot it in Excel to produce a board pack, and share that pack knowing that by the time leadership read it, several of the numbers were already stale.

The data engineering project started with source system audit — understanding exactly what data each system produced, in what format, with what latency, and with what quality. The KYC provider had a well-documented webhook API but the company had never connected it to anything downstream. The transaction monitoring tool had a PostgreSQL backend that was accessible for read-only queries. The case management system had a bulk export endpoint that produced inconsistent field names across export runs.

Over eight weeks, the team built: ingestion pipelines for all three systems landing data in BigQuery, a dbt project with a customer timeline model, an alert lifecycle model, and a case resolution model, and a Holistics dashboard giving the MLRO and compliance operations team live visibility into every metric described above. The board pack that had previously taken two hours to produce manually was replaced by a scheduled PDF export from the dashboard — no manual effort, numbers updated hourly.

The unexpected finding from the first month of live data: one transaction monitoring rule was generating 68% of all alerts but had a true positive rate of under 2%. It had been deployed 14 months earlier and never reviewed. Disabling it cut the alert queue by more than half overnight. That is the kind of insight that is invisible when your compliance data lives in a case management UI and spreadsheet exports — and obvious the moment you have a proper analytics layer.

For fintechs building on top of card infrastructure or managing merchant relationships, the compliance data model intersects closely with other operational datasets. If your business involves card issuing, our post on card programme analytics covers the transaction data model in detail — much of which directly informs your AML monitoring layer.

Frequently Asked Questions

Q: What data sources should a fintech connect to build a KYC/AML analytics layer?

A: The minimum viable set is your KYC provider (identity verification decisions and outcomes), your transaction monitoring platform (alert triggers and alert metadata), and your case management system (case open, disposition, and closure events). Adding a sanctions and PEP screening feed and a SAR filing log gives you full compliance funnel visibility. All of these should land in a centralised data warehouse — BigQuery or Redshift — where they can be joined on a common customer identifier.

Q: How do you reduce AML false positives using data analytics?

A: The first step is measurement — building a per-rule breakdown of alert volume, true positive rate, and false positive rate by joining alert trigger data to case disposition outcomes in your data warehouse. Once you can see which rules generate disproportionate noise, you can calibrate thresholds, retire underperforming rules, or introduce ML-based scoring to supplement rule-based alerts. The calibration exercise is only possible if your data model preserves the full audit trail of alert-to-disposition linkage.

Q: What is perpetual KYC and what does it require from a data architecture perspective?

A: Perpetual KYC replaces periodic static reviews with continuous customer due diligence — refreshing risk profiles in response to real-time signals like transaction pattern changes, sanctions list updates, or beneficial ownership changes. Architecturally, it requires event-driven data ingestion (not just scheduled batch pulls), a customer risk score modelled as a time-series entity rather than a static field, and triggers that can initiate re-review events programmatically when upstream data changes.

Q: How should fintech compliance metrics be defined to satisfy regulators?

A: Compliance metrics — false positive rate, onboarding pass rate, SAR filing latency, case resolution time — must be defined once in a governed semantic layer (typically a dbt model) and referenced consistently across all dashboards and regulatory reports. When a regulator asks how a metric was calculated, you need to be able to point to a documented, version-controlled model definition, not to a spreadsheet formula owned by one person. Consistent metric definition is both an audit safeguard and an internal alignment tool.

Q: At what stage should a fintech invest in compliance analytics infrastructure?

A: Earlier than most do. The incremental cost of building a proper compliance data layer at Series A is small relative to the cost of retrofitting it at Series B when volumes have scaled and regulatory scrutiny has intensified. The minimum viable investment is: a centralised data warehouse, ingestion pipelines from your core compliance systems, and a dbt project with a governed customer and alert data model. This foundation enables all subsequent analytics, reporting, and automation work without requiring a rebuild.

Compliance data is one of the highest-stakes analytics problems a growth-stage fintech faces — the cost of getting it wrong appears simultaneously in your onboarding conversion rate, your operating cost per case, and your regulatory examination outcomes. At Fintel Analytics, we have built compliance analytics infrastructure for payments companies, neobanks, and embedded finance platforms across multiple jurisdictions — from source system audit and data model design through to production-grade dbt pipelines and live compliance dashboards. If your compliance function is still running on manual exports and the MLRO's gut feel, that is a fixable problem, and the fix pays for itself faster than almost any other data investment you will make this year.